Image Credit: Martin Holladay

More Guest Blogs

[Editor’s note: Roger and Lynn Normand are building a [no-glossary]Passivhaus[/no-glossary] in Maine. This is the 15th article in a series that will follow their project from planning through construction.]

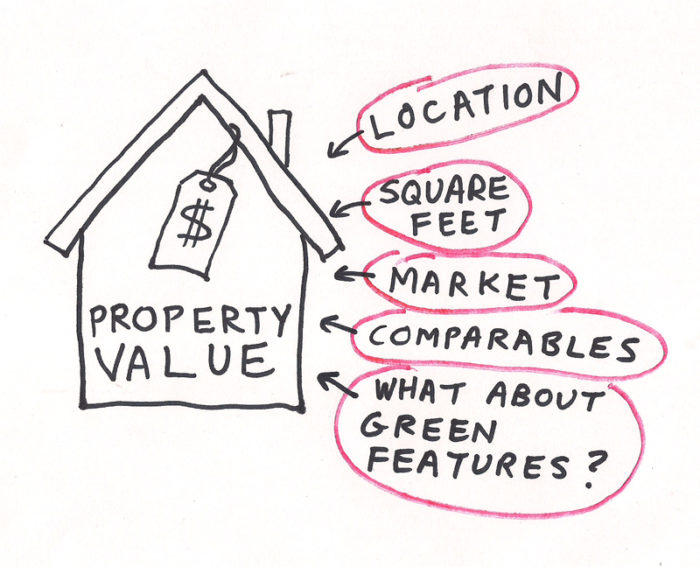

I am seeing “red” on what’s supposed to be a “green” residential property appraisal.

No, I’m not color blind, although my wife Lynn says I am “seriously color challenged” for my occasional fashion faux-pas. Perhaps so.

I’m using figurative colors here, as in getting a property appraisal to recognize and realistically value the energy efficient and environmentally friendly (a.k.a. “green”) aspects of EdgewaterHaus. I’ve turned an irate “red” from an appraisal that ignored all of these features in our home design.

Come on — having no energy bills has to be worth something

You see, our appraiser rated as “typical” the energy efficiency of EdgewaterHaus and four other comparable properties, including one LEED Gold home. He did not recognize or value that EdgewaterHaus is designed to the Passivhaus standard, which results in a home that uses 90% less energy for space heating and cooling than a conventional house. Nor did he recognize or value that our house will seek LEED Platinum status for environmentally sustainable design, or that the design includes a photovoltaic system to get to net-zero-energy use on an annual basis.

This means that our annual energy cost for heating, cooling, lights, laundry and cooking will be zero! We have essentially prepaid the energy costs for much of the building’s entire usable life in the form of an upfront investment in a very tight building envelope. I am aware of only one other home in Maine that can boast this pedigree (the Belfast Passive House). Surely attaining net zero has real, measurable value in today’s real estate market!

Not according to the appraisal we received.

Before lending money, a bank needs an appraisal

I figure we are like the the 99% of the U.S. population who need a construction loan to finance building a new home. We looked at a variety of local and national banks and credit unions, here in southern Maine where we will build EdgewaterHaus, and back in our current home in northern Virginia. We found that “the big guys” like the Bank of America have abandoned construction loans in the wake of the mortgage market meltdown. We concluded that Saco & Biddeford Savings Institution, a small bank with six locations in the area, had the best rates and customer service. S&B savings has been in business since 1827, and their loan officer has been especially supportive of our very green home design.

Along with the usual review of assets, liabilities, and credit scores, all financial institutions will insist on getting a real estate appraiser to look at the construction plans to evaluate the potential market value of the planned building and lot before committing to a loan. If we default on the loan, the lender wants to ensure that it can recover its investment by selling the property.

Are there any “comparables” nearby?

We discussed with the loan officer the challenge of equitably valuing green properties. The economic downturn of the last few years means that there has been far fewer property sales to establish comparable values across similar sized homes and neighborhoods. Nationally recognized green building standards have only emerged in the last five years, so there are few homes or commercial properties that have been built to these standards. Even fewer of these green buildings have been recently bought or sold.

Property appraisals typically value properties based on comparative sales prices, cost of construction, or on income generation potential. We were told that most banks place greater weight on comparable sales, which relies of the appraiser using realtor’s multiple listing service (MLS) database to find the ”comps.”

We knew that finding green property sales comps would be very hard. MLS does not now have any green data fields or green reporting standards, so how would an appraiser find a green building in MLS, if one existed, other than perhaps a green word search in the MILS property description? I have read that MLS is working to develop such fields, but they don’t exist today.

“Soft” greenies and “hard” greenies

And what makes a property green? There are a handful of green building standards. Some (like Passivhaus) are based on building science principles, use an exacting energy model, and require a blower door performance test after the construction is completed to confirm that the building assembly attained the modeled performance standards. Other green standards feel more like a “greenwash.”

More importantly, how do you value green on an appraisal?

I distinguish between two shades of green. There’s the “soft” greenies – those people who will be drawn to buildings that use sustainable materials, use products with recycled content, and products that reduce or eliminate air emissions out of concerns over global climate change. You either believe in the importance of these things or not. Count me as one who does. I would be willing to pay more for a property with these attributes, but I also know that many would not be so inclined. (Hey, some people still don’t believe the Surgeon General’s warnings that smoking cigarettes causes cancer).

Then there are what I call the “hard” greenies – those people who focus on energy-efficiency upgrades and can quantify in dollars the real life value from investing in a very tight building envelope. The hard greenies may embrace some or all of the soft greenies agenda, but it does not drive their singular focus on energy efficiency.

For example, a soft greenie would object to using foam insulation formulated with ozone-depleting chemicals. The hard greenie may view the higher R-value in a one-time application a reasonable tradeoff. In the absence of MLS data, valuing the soft greenie home in real dollars remains subjective, whereas valuing the hard greenie home can be an objective and quantifiable analysis.

On what is the appraisal based?

So here’s the challenge for appraising green properties: less overall residential sales data than previous years due to the economic downturn; a variety of recent green building standards, some more credible than others; few green homes that have been built; even fewer green buildings have been sold; no easy way to mine green attributes in the MLS comp sales data.

So it impossible to appraise a green property? Absolutely not!

Don’t despair. And don’t give in when an appraisal fails to recognize or value legitimate green property enhancements. In fact, I’m pleased to say that major building industry valuation sources have risen to the challenge and have developed credible tools to equitably evaluate green buildings. The challenge is not so much an absence of tools, but the need to educate appraisers and lenders on the use and value of these tools.

I’ll explain what are these tools and how they should be used in my next blog. (After you’ve read Part 2, you’ll probably want to read Part 3 as well.)

The first article in this series was Kicking the Tires on a Passivhaus Project. Roger Normand’s construction blog is called EdgewaterHaus.

Weekly Newsletter

Get building science and energy efficiency advice, plus special offers, in your inbox.

15 Comments

Comps killed us too

We had a similar experience. Although our appraiser was interested in green building and renewable energy investments, he said his hands were tied. There were simply no comparables in our area. The most frustrating part is that if someone wanted to buy our house at a price we both considered fair, they would have to put a large portion of purchase price down in the deposit, because the bank would not finance 80% of the asking price. The only positive, it lowers our tax burden. We wrote about our experience here... http://uphillhouse.wordpress.com/2012/02/25/green-home-appraisal-blues/

Thanks, Roger

Of all the topics you've covered, Roger, this one might be the most valuable for the wider audience here at GBA. It's an issue we've all been aware of and I applaud you for both pushing it and for sharing what you've learned - I anxiously await the next installments.

Energy audits

The results of energy audits, and perhaps any upgrades that were performed in response to a first round audit, would be an objective source of data that an MLS appraisal could use to quantify value with respect to typical energy use by neighbors in the same region. Seattle City Light has been providing energy consumption rankings for its customers and 100 of their respective neighbors with similarly sized houses. It's strikingly effective at making you think about your energy use habits. Audits would be more reliable means of determining energy efficiency of a given house because it would put use patterns on a level playing field. The results of the audits would need to be presented with a standard template with a universal scoring method. If the federal government would sponsor a program to subsidize energy audits, this could quickly build a big enough database for the MLS to tap into. This in turn would motivate home sellers to make energy efficiency upgrades in order to be competitive in the market, especially in those areas of the country where energy is more expensive.

Comfort

Comfort is an aesthetic value that appraisers don't often take into consideration. When I first started building passive solar straw bale homes, 20 years ago, each client would exclaim, this is the most comfortable home I have ever lived in. Since then, I have used that as a selling point for spending the few extra dollars on the energy efficiency. Every appraiser should have a check box for comfort on their list of features of a home.

Seein Red....

Roger, both the the National Association of Realtors (NAR) and the Apprisal Insitute (AI) have begun to see the value of high performance homes. NAR has developed a "Green MLS" tht can be adopted by local MLSs. Check out Green MLS Tool Kit. Similarly, the AI has devleoped a Residential Green and Energy Efficiency Addendum form that can be used by appriasers to document the benefits of a high performance home. Of courese, the trick is to get your local realtor organization and apprisiars to adopt both in their local areas. I also understand that you can request the lender to re-do the apprisal if the appriser is "unqualified" to perform the apprisal -- i.e., document the value of a high performance home's features. I recommend you take this up with the locals. Several realtor associations have adopted a "green" MLS, and apprisars (with a big push from AI) are beginning to understand the value of a high performance h ome.

Whose ignorance?

If the expected selling price does not reflect the low energy costs to run the house, we can't necessarily blame it on the appraisers for their ignorance on the subject. Ultimately, the appraisal is supposed to reflect what the buyer would be willing to pay. If the net zero aspect of the house has no value to the buyer, that's his ignorance at work. If the realtors don't emphasize the energy aspects, that's their ignorance. Realtors ought to bone up on the subject so that they can push very low energy costs and more comfort as selling points.

how to win at home appraisal game

We went through this very nightmare just 1 1/2 years ago. Seems like very little progress to date. We found out (the hard way) that you as the home owner, who is paying for the appraisal have the right to check on the credentials of the appraiser assigned to you. You can't actually choose the appraiser however. In the pre bubble days banks could directly call up their favorite appraiser, however this led to abuses. ("Hey Joe, we'll give you this appraisal job if you can make come in at______). Now your bank has to call an independent appraisal borkerage who will then contact an appraiser. The bank is no longer permitted to have direct contact with the appraiser. The bank does however choose a apnel of appraisers that they will use.

The home appraisal industry has changed markedly over the last 10-20 years. Essentially it has becomeanother victim of the "big box" approach. Several company's that work with large national lenders drove down the cost (prices paid to appraisers). The result was that well established, experienced appraisers wouldn't work for those wages...typically less than 1/2 of what they had been getting. So who would work for these new giant, new inexperienced or inept appraisers.

Currently you best option to avoid such nightmares is to request an appraiser who is a member of the Appraisal Institute. They represent the cream of the crop. You'll pay more, however you can hold them to AI's policy's on evaluating green/energy efficient home. I actually downloaded this information and provided it to each appraiser. AI has a champion of green home appraisaing, her name is Sandra Adomatis, she often has a both at NAHB's green conferences.

She woould heartily agree that the heart and soul of appraising are the comps, be there in lies the problem. What do you do when there are no comps in your area, which is almost always the case? Her answer is that the appraiser MUST then look outside their area to access how green homes sales have compared to convential building stock. Fortunately the Green MLS has been in existence in a few areas for some time, most notably Portland, OR. The Earth Advantage Institute has kept ongoing records of how this has gone, so has Seattle. Also there has been a recent large California survey demonstrating that houses with PV panels sell for more. I saved the appraiser the work of finding all this information and provided them with an email to all the links supporting this, and believe it or not it worked!

When you're on the cutting edge (pun intended) you'll also have to be on the forefront of educating the appraiser as well. They key is letting the lender/brokerage that you'll beexercising your right to review the qualifications of your appraiser, and since it is such a demanding one that you will pay the extra for a member of the Appraisal Institute. By the wasy, I am not an appraiser, however my best buddy is and helped me navigate this tricky waters. Good luck!!!

Energy Efficiency Evaluation Suggestion

I’ve seen/heard of this time and time again, an individual builds the most energy efficient home they can only to have the effort be unrecognized by appraisers and mortgage lenders.

Appraisers do make adjustments to value based on the slight differences in the comparable sales comps used to determine value, lot size, square footage, age, single car garage vs. two cars etc. While these “comparative home sales” do not offer utility cost comparisons (heat, cooling, elect consumption) there is a means to bring this into the evaluation which is currently being used in a slightly different way.

EEM’s (Energy Efficient Mortgages)( tinyurl.com/E-E-Mortgage) are used to increase the home buyers Debt-to-Income Ratio (DTI) to purchase an energy efficient home or make energy improvements. Generally home utility costs are not considered in the DTR lending ratio. The EEM utilizes an established method through an energy audit to determine an annual cost savings projection. Like the real estate appraisal, the energy savings are based on a model of a similar home and uses local utility rates and standard usage rates for the home size. While EEM’s assist the buyer to purchase or qualify for a larger loan to upgrade a homes’ efficiency, it is not currently part of the home value appraisal process.

I am suggesting that there may be a means here utilizing the EEM data and apply it to both the home value appraisal as well as the mortgage (borrowers) side. The project (monthly/annual) energy savings could be multiplied by some factor, say the mortgage term (15-20yr) and that added to the home appraisal. Say a typical homes utility expenses in a given location were $4,500/yr., projected energy savings based on the EEM/Audit were 60%, and mortgage term were 15 yrs. The formula would look something like $4,500 x 60% x 15yrs = $40,500 added value. While this does not take into account increases in fuel costs over the 15yrs, let’s call that a “margin of error”. NOTE: One flaw to this method is the artificial “5% of home value cap” for energy improvements placed on the EEM loans by FHA/HUD/Fannie Mae. This cap needs to be changed for both the EEM financing and the appraisal method I’m suggesting above, as well as for the Energy Efficient Home Building industry/market as in general.

While this EEM formula and estimating method may not reflect the hard costs of various home improvements and/or mechanicals, you will never get the appraisal industry to try to compare the unique energy improvements of solar installations or unique wall constructions their valuation’s . Might as well stick to something more understandable to buyers, lenders and appraisers alike, energy costs and savings.

Blue notes on appraising green

Thanks Roger for posting your story about this common experience of folks who are looking to finance new construction, a purchase, or remodel of a high performing or energy upgraded home.

I’ve added your story to my collective list of “shouldn’t have to be”.

With limited time tonight I’ll chime in on a few notes.

Fewer than 1% of real estate pros; appraisers, agents & lenders, have even begun to seek green expertise. For those who are interested, it’s tough because what they need is difficult to find. Training is as scarce as market evidence of high performing homes. How much time & effort (if training was to actually be available), would it take for an appraiser to develop green expertise? It’s not a 2 hour class! Many, like other trades & professions, have been in survival mode for the past few years so they don’t choose to study what is perceived as ‘non-essential’. We have a ways to go.

Market evidence is required by underwriters. If a house were to default today and the home were listed for sale, what would the market pay? Within typical marketing time of, for example, 30+/- days? Appraisers are called to report what the market will support. The primary source is direct market evidence found in recently sold, similar, comparables.

But what if zero comparables exist?

As Roger noted, tools exist for appraisers to use beyond our typical methods. I’m interested in what tools you’ll be citing.

It is possible to develop a case for valuation based on several approaches to value, supported by secondary market evidence. I led a valuation study last year that appraised 3 energy upgraded homes in Los Angeles (for Energy Upgrade CA). In query of “Do energy upgrades add value?” we determined pre & post upgrade values. We found zero comparables but the resulting green premiums for these 3 ranged from 6-9%. The families were living in these homes so they were not sold. This year we are continuing the study with 4 homes that will be E upgraded & sold. This will provide much stronger evidence. Here’s a link to an article about Part 1 http://tinyurl.com/6osy7eq.

An appraiser might do a terrific job and build a strong case, then the underwriter may not be attuned and reject the appraisal. With the current economic climate, the frequency of red flagging is higher than ever for any element in an appraisal that is ‘atypical’.

2 reasons why market evidence is tough to find for high performing homes, particularly E upgraded existing.

1- Home performance contractors are doing a terrific job! HOs who have experienced living in an EE home treasure it & don’t want to sell. Turnover is low.

2- Data that is accurate & accessible is scarce. Training is needed for agents. As of today there are 800+ MLS systems in US and only (approx.) 17 are relatively ‘greened up’ . Even w/ those, accuracy in reporting , standardized terms, the myriad of green ratings etc- all in infancy with room for improvement & plenty of confusion.

Most folks would agree, easily, that an energy upgraded home is worth more. It makes sense to them. They see the higher quality, lower operating expenses and if they know a bit more, the comfort and indoor air quality benefits. But our data of those who have actually paid more is yet to be commonly discovered.

Energy savings can be quantified. It produces a number appraisers can use. The present value of a future income stream.

Non-energy benefits are more difficult to quantify but appraisers need to find a way recognize these. How do we monetize health? There are ample studies of commercial properties that indicate the financial gains from NEBs far exceed the financial gains from the energy savings (one recent study reported 112X more) . We need further consideration of the value of these benefits in the residential sector. For example: one of the families in Part 1 (study referred to above) has 3 sons who suffered from asthma. When the upgrades were installed their symptoms were remarkably reduced. They were not expecting this benefit but it’s what they’re most thrilled about. What is the value of improved well being? More days in school, participation in sports etc, less medical related expenses.

What are the real benefits of a high performing home? How is this reflected in the price folks pay?

What are the real costs of owning a home? RE agents with green expertise can help guide shoppers to ask different questions.

I haven’t seen that we have as much a problem with green washing or over selling as much as underselling. Even with an extensively E upgraded home, agents are not often ‘selling’ the assets or clearly stating. We have the blind leading the blind. If the shoppers are not made aware of the asset differentials…how can they choose between an apple & orange if they don’t know an orange is an option & how it looks, tastes, smells.

I’m involved in outreach and training of these topics- green building/HP including approaches in valuation- to this group, the RE pros.

I see a gap of disconnection between the RE pros and the general home owning/shopping public. Their lack of training is hurting the green home market.

When ordering an appraisal, request that the assigned appraiser has expertise or ‘competency’ appraising this type property. Help the appraiser clearly understand the assets with related docs, contact info of contractors, BPI or HERs test out results, utility records and a list of scope of work.

Debra Little

Dick "If the expected

Dick "If the expected selling price does not reflect the low energy costs to run the house, we can't necessarily blame it on the appraisers for their ignorance on the subject."

You can't say the appraiser is ignorant if there is not a recognized market for efficient homes.

As a former appraiser I can say there are several issues in getting an appraisal to reflect unique properties.

For starters cost does not equal value. You can build the biggest and nicest house but that doesn’t mean someone will pay what it costs to build. A pool is a good example. In many parts of the country you can spend $30,000 or more on a pool and see very little if any increase in value.

The biggest obstacle is that appraisers do not assign value. When I hear these arguments it comes down to the appraiser wont give me what it costs to build. The appraisers job is to collect market data and to provide a supportable estimate of the value of a home. If there is not any market data to support an adjustment then you or the appraiser cannot prove there is market value for the energy efficient features. It’s all supposition.

Another issue is the state of the lending and appraisal climate. The big banks starting with Wells Fargo, Bank of America, etc have created another profit center that handles the ordering and receiving of appraisal. They have driven down prices paid to the actual appraiser and in turn have lowered the quality of appraisals. They use the lowest cost appraisers and many of them are not qualified to due a complex appraisal.

Another issue is the time it would take an appraiser to do the market research and gather data. It would be much more time consuming and should cost much more than a standard appraisal. I doubt the lender would pay what it would take to complete a difficult appraisal. The appraisal fee would likely be in excess of $1,000 not including the lenders markup.

There is also the issue of who should assume the risk of the loan. As a lender I would not want to make a loan on a property that I did not know what it would sell for in case of foreclosure but that is what many are asking the lender to do.

From appraisal standards market value is defined as a home that has been exposed to the market with a buyer and seller agreeing to a price. A custom built home does not meet this definition. A custom built home does not provide any usable market data that can be used by other appraisers. Market data is not created until the owner lists and sells the home. Market data can be a problem for new custom home neighborhoods.

Until the market catches up the solution may have to come from the lenders creating programs that take a base appraisal without energy efficient features and making an "administrative" addition to account for the saving. The borrowers should be expected to have more equity and be a bigger partner.

Appraiser classified us as "unconventional"

We recently had an appraisal done on a superinsulated house we are planning to build. The value the appraiser arrived at was what we had hoped but, because we won't have central heat (just a woodstove and ductless mini split heat pump), he made a note that the home is "unconventional." Consequently the bank will not be able to sell our mortgage and we will be forced to pay a higher interest rate. I refuse to pay thousands for a heating system that we won't need just to save those thousands over time on our mortgage, so this is really unfortunate. The appraiser said that he has seen a couple of other homes with similar designs, but at this point they are still too rare to be generally accepted. We are working with an engineer who has assured us that the house will heat evenly throughout and would not benefit from central heat... but apparently the average home buyer can't be convinced of this fact.

response to Randy George

I agree Randy, that was an unfortunate and in my opinion, misguided decision by your appraiser. You do have the opportunity to request a reconsideration. An appraiser trained with green expertise would have understood the benefits of your system. He may not have been able to clearly support added value (though that case might be made) but should not have imposed a negative. Did he ask about your projected energy savings and calculate those?

Debra Little

Debra

The problem is not the

Debra

The problem is not the appraiser. A person can take a point counter point on this issue. First off we can not look at individuals but we have to look at the larger market. If you were to build the home and put it on the market what would be the reaction of buyers. I for one would like to know that all areas of the house are usable. I dont want a room(s) that are too hot or cold. How do I know is going to be the case. Given that each house is unique its hard to say how a house will perform. Although the home may meet the needs and expectations of the original owner it may not receive the same acceptance to other owners.

I also get the sense of entitlement from many borrowers. Before the era of out of control lending the mortgage industry develop a set of lending policies reduced the risk of lending and help control the loses. Then we forgot those lessons and used the mortgage industry to drive our economy. This lead to the collapse of the mortgage market. and substantial damage to the overall economy.

I think asking lenders to gamble on the value of homes is not a wise thing to do. I agree with energy efficient building but at what point do cost's exceed the benefit. I dont think we know these answers.

The question is who should bear the risks. Should it be lenders/investors, taxpayers (not in favor of) or should the individual assume the risk.

Unconventional House

Randy,

A simple solution would be to add electric resistance heating to your house plan. This would satisfy the lender and appraiser, a backup heating system is desirable for many.

Superinsulation is a great way to build and the value may only be apparent to those who live in such a home. That current lending practices do not recognize energy efficiency is unfortunate and shortsighted. I contend a highly efficient building is also a very well built structure, efficiency does not happen accidently. Site planning, thick insulation, proper window placement and favorable surface to volume ratios all help lead to a succesful building project

Building better will lead to customer loyalty, comfort is hard to define but we all strive for it. A house is worth what someone will pay for it, a solidly built and well designed structure will bring a better price in the marketplace.

Appraisal Value

As an appraiser in the NE it is difficult to determine contributory value to 'green' components of a home. In Ct there is a very small number of high performance homes. There are studies out there that help appraiser estimate this contributory value. It may not be 100% of the cost but there is value. The Appraisal Institute has info and members, like myself, who can help property owners.

Log in or create an account to post a comment.

Sign up Log in