More Guest Blogs

You worked hard. You saved up a down payment. You bought your dream home in a good neighborhood with good schools. You finally “made it.” And then one day your house floods and you have four feet of standing water in your living room.

As you start the long process to rebuild, you learn from a neighbor that the house has flooded before. The seller never told you. Why? You live in one of 21 states that have no statutory or regulatory requirements that a seller disclose a property’s flood risk to a buyer.

You thought you knew everything about your house, but the deck was stacked against you. Your state did not require the previous owner to tell you that the biggest financial investment of your life has flooded and is at risk of flooding again in the future.

“Buyer Beware” is a recipe for disaster

In too many states, home buyers are kept in the dark about a property’s vulnerability to floods. Buyers may only learn about that risk at closing when their lender notifies them that they need to buy flood insurance. Others only learn of that risk after their new home is flooded.

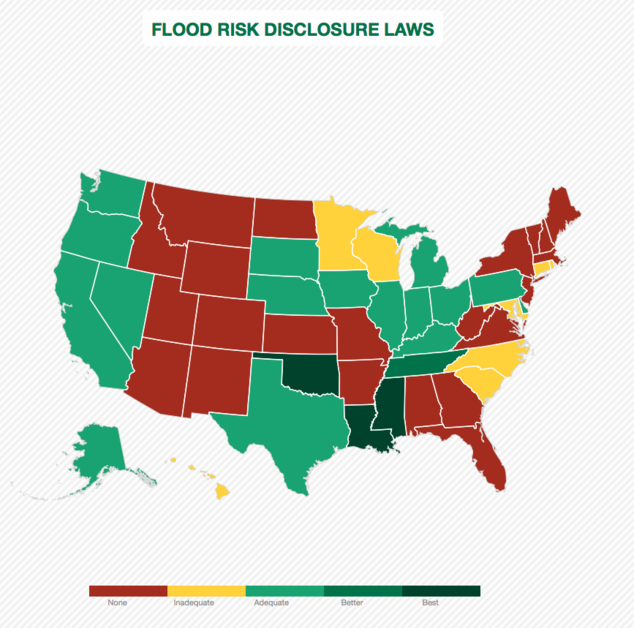

In 21 states, there are no statutory or regulatory requirements that a seller disclose a property’s history of flood damages to a buyer. Sellers are also not required to disclose whether the property is located in a floodplain. The other 29 states, plus Washington, D.C., have a smorgasbord of disclosure requirements, many of which can hinder buyers from making fully informed decisions. The Natural Resources Defense Council and Columbia University’s Sabin Center for Climate Change Law reviewed all 50 states’ real estate disclosure laws and found that in many places, home buyers are not given the information that they need to make informed decisions about whether they should buy a house, which is a major financial investment.

Explore the interactive map for each state’s disclosure law report card.

States with some of the worst grades include Missouri, Florida, and New York. For example, Missouri, known as the “Show Me State,” received an F, as the state has zero statutory provisions that would require a seller to tell a buyer whether a house has ever flooded.

In fact, Missouri has almost no codified requirements for what a home seller must disclose to a potential buyer other than whether the property was ever used for the production of methamphetamine. As a result, Missouri home buyers are disadvantaged when it comes to learning of a home’s flood history, which is a problem as Missouri is all too familiar with the damage that can be wrought by flooding.

Home buyers in Florida, a state with enormous problems from flooding and sea level rise, are also not entitled to information about flooding. Florida, like Missouri, has no statutory or regulatory requirements for a seller to disclose a property’s flood risks or past flood damages to a potential buyer. As such, Florida received an F as home buyers are greatly disadvantaged when it comes to learning of a home’s flood history or potential for future flooding. Given that almost 30 percent of Florida’s buildings are located in a 100-year floodplain, there is a high likelihood that buyers are going to be swamped due to a lack of statutory disclosure laws.

New York received an F. Its disclosure law contains a major loophole making it no better than the other 21 states that do not have flood hazard disclosure laws on their books. While New York’s disclosure statute states a seller must disclose whether the property is located in a designated floodplain, the same New York law also acts to allow the seller to simply pay a $500 credit at closing to avoid having to provide a disclosure statement.

Many disclosure laws fail to fully inform buyers

Even in states that have flood hazard disclosure laws, home buyers may not learn the full extent of a property’s flooding problems. For example, in Iowa and Texas, two states where major flooding has occurred, sellers are only required to inform buyers whether the property is located in a floodplain and whether they know of any previous flooding problems at the property. However, neither state has a specific requirement to disclose whether a property is mandated to be covered by flood insurance.

So, for instance, if past owners received federal disaster aid, there is a legal requirement for all future homeowners to purchase flood insurance. That information may not be disclosed at the time of purchase by the new owner. They may not find out about this requirement until their home floods, they apply for federal disaster aid, and are denied because they failed to purchase flood insurance.

While Texas law does require disclosure of whether the current owner carries flood insurance, this disclosure requirement does not address situations where flood insurance is mandatory and the seller has dropped coverage in violation of federal requirements.

States must require that owners disclose a property’s flood history to a buyer. If a property has flooded once, it will likely flood again, and the likelihood for floods to occur is increasing in most regions of the county.

What should buyers have a right to know?

We cannot expect home buyers to make good decisions if they are denied information. States should have disclosure laws that ensure that persons selling a property disclose the following information:

- Whether the home has ever been damaged by a flood and the extent of the damage;

- Whether the home is located in a floodplain and, if it is, the flood zone classification (100-year or 500-year) of the property and the source and date of this information;

- Whether the seller and/or previous owners ever received federal disaster aid that would require all future owners to obtain and maintain flood insurance on the property and, if they have, the type of aid and amount received.

However, such disclosure and transparency provisions should not be limited to disclosure requirements imposed on sellers. The National Flood Insurance Program (NFIP) must also improve the information that is available to both home buyers and homeowners.

Current homeowners who have not had the luxury of living in a state with good flood hazard disclosure laws should have a right to know about their property’s flood risk. This should include any past history of flood insurance coverage, damage claims paid, and whether there is a legal requirement to purchase flood insurance because of past owners’ receipt of federal disaster aid. This is information that Federal Emergency Management Agency should have if a property was ever covered by the NFIP.

Congress is not without ideas on how to fix such issues. The House passed the 21st Century Flood Reform Act (HR 2874) last November. The bill contains multiple proposals that would provide current and prospective homeowners with a right to know if the property in question has a history of flooding. It would also provide the broader public, including federal, state, and local officials responsible for hazard mitigation, a right to NFIP data related to assessing flood risk.

For example, Section 108 – Availability of Flood Insurance Information Upon Request is a solid start. Per this section, Representative Sean Duffy has sought to provide homeowners a “right to know” about their property’s past flood insurance claim payments and flood damages. In addition, a homeowner could find out whether they may be required to purchase flood insurance due to receipt of federal disaster assistance for their home by a previous owner.

Providing property owners better access to their property’s flood history could help encourage homeowners to consider purchasing and maintaining flood insurance or undertaking mitigation actions to lower their property’s flood risk. The potential for encouraging better decision-making is why NRDC has long called for including a homeowner “right to know” provision in the NFIP.

Additionally, Section 109 – Disclosure of Flood Risk Information Upon Transfer of Property addresses the problem of flood hazard disclosure laws at the state level. Representative Ed Royce put forward a proposal that would require sellers of a house to disclose past flood damages to potential buyers. This proposal would have an impact nationwide as states would be required to enact sufficient flood disclosure laws in order to remain in the NFIP.

Nationwide disclosure requirements are not uncommon. The federal government uses a similar mechanism to ensure that states require that sellers disclose other health and safety risks, like the presence of lead-based paint. As flooding is the most common natural disaster in the United States, disclosure of flood risk makes sense both from a public safety standpoint and a fiscal standpoint.

And states need not reinvent the wheel to enact good disclosure laws. There are states that have good disclosure laws. Louisiana, a state that has incurred more flood damages than any other, requires that home buyers be well informed about the risks they’re taking on when they purchase a new home. In Louisiana, a seller must not only divulge detailed information about past flood events and whether the home is located in a flood zone, but the seller must also tell the buyer whether any previous owner was a recipient of federal disaster aid that would require a new owner to obtain and maintain flood insurance on the property.

Greater transparency protects people and property

The lack of disclosure regarding flood hazards is problematic. Too many Americans have no knowledge of a home’s flood history or flood risk before making one of the biggest financial investments of their lives. Given that floods are the most common and costly disaster of Mother Nature’s wrath, a lack of information in real estate transactions about that risk is a significant problem — one that is not only burdensome to those that unknowingly buy such a property, but also federal taxpayers who often foot the bill for rebuilding flood-damaged areas by bailing out the NFIP.

Joel Scata is water and climate attorney with the NRDC. Research for this project was funded by a grant from the New York Community Trust. This post originally appeared at the NRDC Expert Blog. (Photo: Staff Sgt. Sharida Jackson / CC / Flickr)

Weekly Newsletter

Get building science and energy efficiency advice, plus special offers, in your inbox.

3 Comments

This story doesn't pass the sniff test.

Mortgage lenders require a flood search and the appraisal is also required to notate whether a property is in a flood zone as well as designate the type of zone. Flood zones (zones beginning with the letter "A" or "V") require that the buyer obtain flood insurance. Also the buyer owns the appraisal so they have it in their possession however the flood search is done behind the scenes.

Of course there are situations where flood maps haven't been updated in a few years and surrounding development caused an area to become susceptible to flooding. That's a rather rare occurrence.

I fail to see how adding yet another piece of paper (which will unlikely be read by the buyer anyways) to the already over-disclosed home buying process will make a difference.

A 5 year old home that has never flooded might have higher risk than a 10 year old home that flooded once. Good flood databases/modeling makes more sense to me.

I would think that a good inspector could discover signs that a house has flooded.

When in doubt, build higher.

1. Lenders order an appraisal and it is owned by them, but paid for by the borrower. The borrower is entitled to a copy of the appraisal.

2. Ask the Realtor or your buyer's agent to find out the flood history and status. Similarly, ask the seller the flood history and status. Send a written letter to your agent and the seller stating that it is your understanding, based on the agent/seller's representations that ......... This gives the agent and seller constructive notice as to their representations.

3. Go to the FEMA website and look up the property address on the flood maps. Check this out:

FEMA Flood Map Service Center | Welcome!

https://msc.fema.gov/

The FEMA Flood Map Service Center (MSC) is the official public source for flood ... or location, the map results now show interactive flood hazard information.

MSC Search by Address · FEMA Flood Map Service · NFHL · FAQs

Log in or create an account to post a comment.

Sign up Log in