More Guest Blogs

Over recent months there has been an orchestrated pushback against investors and insurers who integrate the risks of climate change into their business models. That pushback–emanating from Republican-led states–is having an impact on how companies speak publicly. But whether it will affect their efforts to respond to climate change is less clear.

The latest targets have been global insurance companies, and their responses offer some insight.

Under pressure, several major insurers, including AXA, Allianz, Lloyd’s and Swiss Re, have pulled out of a United Nations-organized alliance committed to a global goal of net-zero emissions by mid-century. There’s a word for companies going quiet in the face of orchestrated attacks: “greenhushing.”

But while the insurers’ departures from the alliance might look like a victory for politicians and political donors who want to delay action on climate change, the companies say leaving doesn’t change their business decisions.

I have worked with businesses globally on sustainable development for over 20 years and follow both what they say and what they do. The insurance industry has obvious reasons to care about climate change and efforts to slow it, starting with the fact that disasters cost them money and the risks are rising.

The assault on protecting the climate

Republicans began targeting so called “ESG investors“–those who incorporate environmental, social and governance performance standards in making investment decisions–a few years ago as ESG-managed assets grew into the tens of trillions of dollars. Texas led the way in 2021 with a law prohibiting state entities from investing with firms that cut their investments in fossil fuel industries.

In 2022, Republican state attorneys general began to go after the Glasgow Financial Alliance for Net Zero, or GFANZ, an umbrella body for insurers, banks, asset owners and asset managers. The influential group had a starting membership of more than 400 financial institutions representing over US$130 trillion of assets under management.

One line of attack accuses GFANZ members of breaking antitrust rules, claiming that when companies participate in groups committed to lowering greenhouse gas emissions, competitors are cooperating in ways that affect prices in violation of U.S. law.

“Net-zero” is shorthand for taking steps to limit global warming to 1.5° Celsius, an international goal to prevent increasingly severe climate damage that is fueling severe storms, heat and wildfires. Clubs have formed across the financial value chain to find solutions. Among them is the U.N.-convened Net-Zero Insurance Alliance (NZIA), a group of some of the world’s leading insurers and reinsurers. Members commit to transitioning their insurance and reinsurance underwriting portfolios to net-zero greenhouse gas emissions by 2050.

In a letter on May 15, 2023, 23 Republican attorneys general took their criticism further and attempted to blame the insurance alliance–rather than the rising cost of disasters like wildfires and hurricanes–for economic ills from rising insurance premiums, fuel prices and inflation.

Facing the threat of lawsuits, whether viable or not, and the potential for reputational harm, several mainly European-based insurers and reinsurers with substantial investments in the U.S. left the group.

The attacks have dampened the public discussion on evolving practices in net-zero pathways and ESG investing, even for those who stay. Fewer firms are keen to draw attention to their progress because, in a global market, the backlash from the U.S. threatens any of them.

GFANZ has stated that the “political attacks are now interfering with insurers’ independent efforts to price climate risk, which will harm policyholders, main street investors and local economies.”

Silencing climate voices, but not actions

However, while the insurers might not be speaking out, their assessment of climate trends hasn’t changed, nor has the impact of those trends on their businesses.

When Lloyd’s pulled out of the alliance in late May 2023, the London-based insurance and reinsurance company made clear that it remains “committed to delivering our sustainability strategy including supporting the global economy’s transition.” It said it continues to support the U.N.’s Principles for Sustainable Insurance and Sustainable Development Goals.

Swiss Re also stressed that it has kept its sustainability strategy the same and that its pullout doesn’t reflect a lesser commitment to climate policies. It remains a member of the Net Zero Asset Owner Alliance.

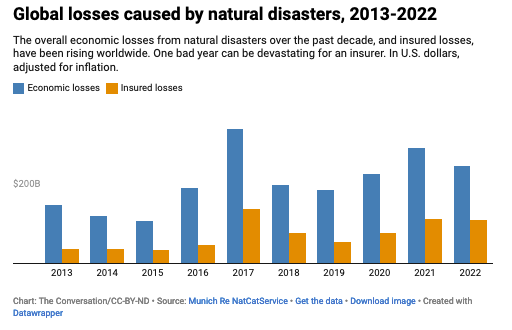

Swiss Re Group’s data clearly shows the reason why. In 2021, some $270 billion in losses were attributable to natural catastrophes worldwide. The $111 billion of those losses that were insured represented the fourth highest payout since Swiss Re Institute, the insurer’s research arm, began keeping records in 1970.

The World Meteorological Organization reports that weather and climate disasters such as floods, heat waves and forest fires have increased fivefold in the past 50 years. These disasters have caused environmental harm, the loss of more than 2 million lives and more than $3.64 trillion in economic damage.

Not talking about these risks doesn’t help homeowners and businesses that rely on insurance, and doing nothing to stop climate change worsens the threats. Some consultants and auditors have started sounding the alarm that increasing natural catastrophes could collapse the insurance market model we know today.

An economy-wide problem

The insurance industry plays a crucial role in the overall functioning of economies. It promotes resilience by providing a safety net against unexpected events, helping individuals and businesses to recover more quickly. It facilitates commerce and trade; for instance, marine insurance covers the risks of shipping goods, ensuring that trade flows smoothly. It also encourages risk-management practices.

Without insurance, disaster costs would fall heavily on individuals and businesses, hindering economic growth and stability.

Already, as climate risks increase, some regions are becoming increasingly uninsurable. State Farm and Allstate cited wildfire risks when they recently announced they would stop selling new home insurance policies in California, putting pressure on outdated regulation of the insurance industry.

Looking ahead

As the United States heads into its long election season, the ESG backlash risks pushing more companies’ transition pathways into the quiet zone and slowing much-needed regulation.

The world is at an inflection point in its climate transition efforts. Capital is shifting to low-emissions technologies and, in some cases, reshaping industries faster than imagined.

Insurers have the ability to accelerate the transition through their underwriting practices and promoting risk mitigation through their substantial investment portfolios. They also recognize that, to protect their balance sheets and for the sake of the planet, society needs to pick up the pace in the transition to net zero.

Rachel Kyte is dean of the Fletcher School at Tufts University. This article was originally published at The Conversation.

Weekly Newsletter

Get building science and energy efficiency advice, plus special offers, in your inbox.

4 Comments

Stop with the political hit list! A lot of the so called Environmentalists are nothing more than money hungry con artists. They give a really bad name to the rest of us who do care about the environment. It's time we start policing ourselves and call the con artists out. Democrats will pass anything with the word environment in it so you can kick it back to them in donations.

While I agree that both major parties have their problems, one party is actively working to ignore climate change. I don't see anything in the article that appears to be non-factual. If you want to rebut what was written, go ahead. Crying about one party being unfairly targeted is disingenuous. Dumping the solutions for climate change onto individuals and businesses is in no way going to solve the problem.

The article might not be non-factual but it's language and tone overgeneralize and blur details to divide people on political grounds.

Kyte entitled the article "GOP Targets Insurers". Her evidence is a Republican comptroller in Texas who banned financials who do ESGs from doing business with the State. ESGs aren't banned in Texas generally, and besides there's a known conflict of interest for the comptroller (Houston is the oil & gas stronghold in the US). It's also a stretch to say 1 public official's actions represent the entire GOP. So Kyte's section entitled "Assault" expands to more Republicans via the letter from State attorney generals but this blurs the sequence of events. By the time the State attorney general's wrote their "threat" of lawsuit letter, major insurers had already left the NZIA. Kyte's article makes the reader believe this letter *caused* insurers to leave. It's difficult to disprove happenstance when insurers don't tell us the reason.

So Kyte uses language and a tone to blur events and overgeneralize members from political parties.

I think the State attorney generals have a point that needs to be settled in court. If a bunch of banks got together and decided they were only going to lend money to businesses who make green shoes and not to businesses who make black shoes, called their alliance Green is the New Black, and told depositors that green shoes are better than black, I think a lot of depositors would question whether the banks were genuinely interested in making a return on business loans or trying to collectively drive the price of black shoes.

Obie: So you don't think insurers should be allowed to consider climate change when assessing risk? Because the point of this article is that Republicans object to insurers doing that. Which strikes me as bizarre. Pretty much the most important thing insurers (and reinsurers) do is evaluate risks. Otherwise, they can't price their policies.

Log in or create an account to post a comment.

Sign up Log in