More Guest Blogs

On Dec 4th, 2023, the Mission Possible Partnership (MPP) launched the Making Net Zero Concrete and Cement Possible report, an industry-backed, 1.5C-aligned global net-zero roadmap for the concrete and cement sector, also known as the Concrete and Cement Sector Transition Strategy. MPP is a global movement of climate leaders focused on supercharging efforts to decarbonize heavy industry and transportation. RMI is a founding partner of MPP alongside the Energy Transitions Commission (ETC), the We Mean Business Coalition, and the World Economic Forum (WEF).

This report builds on the Global Concrete and Cement Association’s (GCCA’s) Concrete Future: The GCCA 2050 Cement and Concrete Industry Roadmap for Net Zero Concrete and the European Cement Research Academy’s (ECRA’s) Technology Papers 2022, with input from a wide range of stakeholders in the concrete and cement ecosystem. As part of a coherent set of roadmaps for all heavy industry sectors, the Sector Transition Strategy is anchored in a granular technoeconomic model for how the global concrete and cement sector can reach net-zero by 2050 and comply with the 1.5°C target. Going beyond emission trajectory modeling, the report also provides near-term milestones and recommended actions that various stakeholders can take to unlock the transition in this decade.

The report Making Net Zero Concrete and Cement Possible can be downloaded here, along with the executive summary, infographics, and the interactive net-zero explorer. Want a quick summary of the Sector Transition Strategy? Here are the top five takeaways on the concrete and cement industry’s net-zero transition that you will want to know from this report.

1. The concrete and cement industry can achieve net zero by 2050 with concerted efforts from actors across the value chain.

There is no silver bullet to decarbonize concrete and cement. The report identifies a suite of interventions that are needed to reduce and eventually eliminate sectoral emissions. On the demand side, this includes more efficient use of concrete in construction, cement in concrete, as well as clinker in cement. On the supply side, this includes fuel switching, efficiency improvements, power sector decarbonization, and eventually carbon capture, utilization, and storage (CCUS).

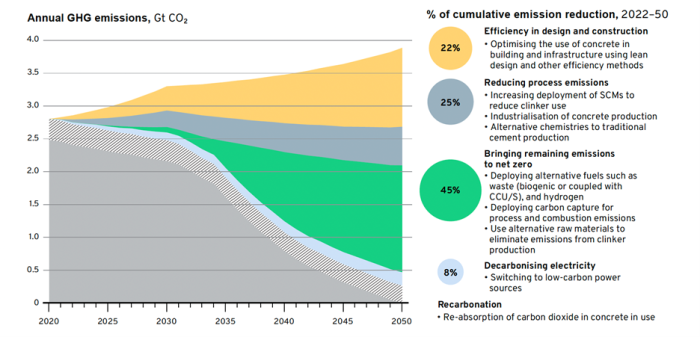

As shown in Exhibit 1, remaining business-as-usual means 98 gigatons (Gt) of CO2 will be emitted from the concrete and cement industry between 2022 and 2050, which is twice as much as the sectoral carbon budget to stay on track of the 1.5 °C target. Among all the interventions needed to bring the industry to net zero, more efficient and effective use of concrete, cement, and clinker (the yellow and dark blue areas below) have the largest decarbonization potentials before 2030. After 2030, CCUS will start to play an increasingly important role in emission reduction.

Exhibit 1. Decarbonization potential of each lever in the net-zero scenario.

Note: Emissions in this figure refer to Scope 1 and 2 emissions. Scope 3 upstream emissions would add approximately 3.8 Gt CO2e of cumulative emissions from 2022 to 2050. Decarbonization of electricity involves electricity use for kilns, grinders, and carbon capture.

The concrete and cement industry is highly localized. Consequently, a nuanced understanding of the feasibility of individual levers at the plant level becomes crucial. Key determinants such as access to raw materials, the infrastructure for carbon storage and utilization, and the availability of low-carbon energy sources play a pivotal role in selecting the best set of solutions.

2. CCUS is critical. But alone, it falls short of achieving net zero and bears inherent risks

The net-zero scenario shown above illustrates that CCUS has the largest emissions saving potential among all technologies. Across all scenarios discussed in the report, CCUS continues to play a critical role and accounts for 35-50 percent of cumulative emissions savings.

However, CCUS is not a magic wand. It is expensive, energy- and water-intensive, and has environmental and social impacts on surrounding communities if not deployed properly. Real-world projects frequently achieve lower carbon capture rates than the theoretical limits, reducing the overall emission savings. In addition, there are many unanswered questions around the best approaches to transport, store or utilize captured carbon. These risks related to CCUS present challenges, particularly for Global South countries with rising concrete demand.

Therefore, the key task for this decade is to deploy the lower-hanging fruits, mainly demand reduction levers, and lay the groundwork for CCUS through research and development, regulation frameworks, investments, as well as carbon transport and storage infrastructure deployment.

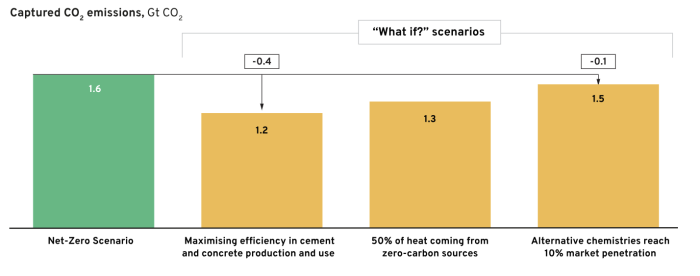

The report shows that faster deployments of other decarbonization levers can effectively reduce the reliance on CCUS, as shown in the figure below. In particular, maximizing demand reduction levers reduces the annual captured CO2 emissions in 2050 by 25 percent, from 1.6 Gt to 1.2 Gt. Similarly, zero-carbon fuels and alternative cements can also reduce the emissions needed to be mitigated by CCUS.

Exhibit 2. Efficiency improvements, alternative fuels, and new chemistries could reduce the captured emissions by 0.1 to 0.4 Gt CO2

Note: These scenarios demonstrate the scale of the interaction between new technologies and CCU/S use. At this early stage, it is difficult to estimate the market penetration rates of these new technologies. Key assumptions: Maximizing efficiency in cement and concrete production and use sensitivity scenario involves a reduced clinker demand by 27% by 2050. Fifty percent of heat coming from zero-carbon sources assumes that by 2050 electricity and hydrogen make up 50% of kiln heat demand. Alternative chemistry scenarios involve a 10% market penetration by 2050.

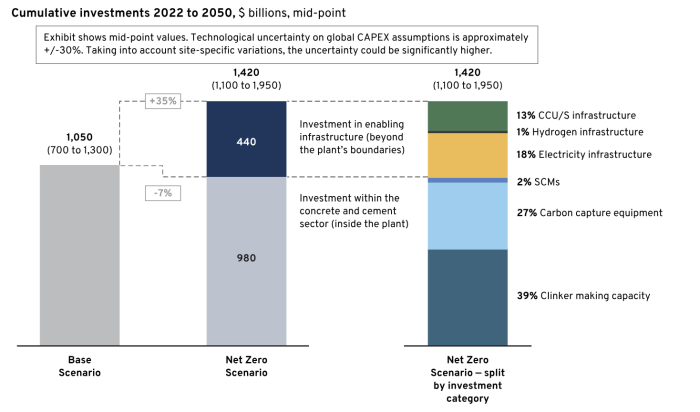

3. Between 2022 and 2050, a $1.42 trillion investment is required for the net-zero transition. Optimized concrete and cement use reduces in-sector investment by 7 percent, while CCUS and clean fuels raise overall investment by 35 percent compared to business as usual.

The report estimates the investment needed both within the concrete and cement sector and outside of the industry between 2022 and 2050 under different scenarios. Investment within the concrete and cement sector includes cement-making equipment, supplementary cementitious materials (SCM) supply chain infrastructure, and carbon capture equipment. Yet the $980 million investment in the sector represents a 7 percent reduction compared to the business-as-usual case, mainly caused by reduced demand for concrete and cement, which offsets the $390 billion investment needed for carbon capture equipment at cement plants.

However, the total investment, including the above mentioned in-sector investment as well as CCUS transport and storage facilities, hydrogen infrastructure and clean electricity generation, will increase by 35 percent from $1.05 trillion to $1.42 trillion, driven by the construction of capital-intensive clean energy and carbon capture infrastructure. Innovative financial instruments and enabling policies are required to channel adequate capital from both public and private entities, ensuring the timely decarbonization of the concrete and cement sector.

It is worth noting that successful deployment of emerging technologies could have significant impact on the investment needs in the upcoming years. For example, producing cement with new chemistries on the commercial scale can reduce investment needed for CCUS, while increasing investment for cement-making equipment and clean electricity.

Exhibit 3. The net-zero transition decreases in-sector emissions by 7 percent but increases overall emissions by 35 percent.

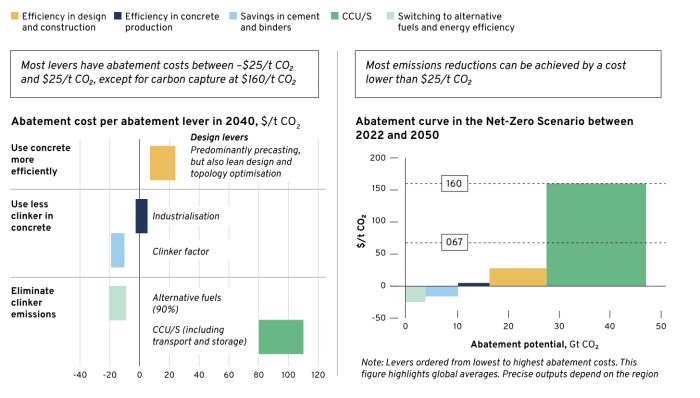

4. While net-zero transition means a 40-120 percent increase in the cost of cement, it will translate to a relatively small green premium in construction.

The abatement cost of all decarbonization solutions as well as the green premium of low carbon concrete and cement are also discussed in the report. The figure below summarizes the abatement costs for different technologies. Levers such as the use of SCMs and industrialization of cement production not only reduce emissions but also potentially save costs. CCUS is the most expensive lever among all solutions, with an abatement cost of $160 per ton of CO2.

Exhibit 4. Abatement cost of various decarbonization solutions

The cost increase for cement is 40–120 percent, driven mainly by CCUS investment, which translates to a 1.5–3 percent increase for construction as cement is a relatively small portion of the total project cost. The cost of the transition will be highly variable, depending on the levers used and plant locations. Premiums are likely higher in developing countries and for concrete-heavy applications such as concrete bridges.

5. Reaching net zero by 2050 requires a portfolio of policy and financial instruments to create an enabling environment for innovation and decarbonization

The year 2050 is just one investment cycle away given the industry’s long-lasting capital assets. Over the next 10 years, major new investments should be net-zero compatible. Decarbonization technologies need to be deployed on a large enough scale to trigger cost reductions and enable significant GHG emissions savings in the following years. This profound transition is not possible without immediate and concerted efforts from across the value chain. Near-term actions required from industry, government, and finance stakeholders include:

- Green public and private procurement programs to aggregate demand for low-carbon concrete and cement;

- Performance-based concrete and cement standards supported by robust testing measures;

- Carbon markets. The two largest cement producers in the world, China and India, have both announced plans to include the cement sector in the national emission trading schemes.

- Fiscal incentives for pilot projects. For example, the Office of Clean Energy Demonstrations (OCED) under the US Department of Energy is providing $6.3 billion to support accelerated industrial decarbonization actions.

- Emission target setting and reporting under frameworks such as the Science Based Targets Initiative (SBTi);

- Clear market regulations for CCUS to ensure a stable and investable market environment.

- Shared carbon management and clean energy infrastructure in industrial hubs. MPP is currently supporting the deployment of two clean industrial hubs in Los Angeles, California and Houston, Texas.

- Invest in low- and zero-carbon cement production facilities from today to avoid being locked into investments in high-polluting assets and prevent the risk of stranded assets.

The Sector Transition Strategy is a roadmap for navigating the concrete and cement industry from where we are today to the net-zero goal. Yet, we won’t reach the destination by simply following the directions. The transition requires a decades-long, step-by-step journey with substantial technology, finance, and policy interventions, as laid out in the report. Effectively translating the roadmap into tangible on-the-ground actions starting from today is imperative to guarantee the success of the net-zero transition.

This article originally appeared on RMI.org on December 19, 2023. It is republished here with RMI’s permission.

Weekly Newsletter

Get building science and energy efficiency advice, plus special offers, in your inbox.

13 Comments

By 2050? What if every year between 2024 and 2050 is a record warm year, will that change the calculation?

Might want to ask China as they are the largest emitter of carbon dioxide gas in the world. 11,000 million metric tons of CO2 released in 2023. The USA shouldn't bear all the weight as it's a global issue. The USA puts out about 14% of the global emissions. That leaves 86% for the rest of the world countries.

That's not even taking into account the present and future wars overseas that will destroy infrastructure and require complete rebuilding with concrete. Just look at the pictures of the destruction in Ukraine and Gaza. Not one wood framed home in the Middle East area. They use masonry everywhere. The amount of concrete required to rebuild will be staggering.

My point is that the USA is doing it's part but the rest of the world needs to step up and do there part. The right way is to support U.S. energy producers. Stop penalizing American-made oil and gas. Embrace American energy production as the strategic national and economic asset that it is.

"the USA is doing it's part but the rest of the world needs to step up"

haha. It's always the other guys fault. USA is number 1 baby. Our history is clean as a whistle. We get a free ride to the top while the developing world pays.

The US has 4.3% of the world's population but 14% of global CO2 emissions. China has twice our emissions but more than four times our population: https://www.worldometers.info/co2-emissions/co2-emissions-per-capita/.

"A 40-120 percent increase in the cost of cement" plus the yearly inflation increases will be a tough pill to swallow for future home buyers. I was paying $150 a yard for concrete in 2017/2018 and now it's at $210 a yard in 2023/2024 ( a 40% increase in just 5 years). An 80% increase would bring it to $378 a yard. You got footings, stem walls, basement walls, house & garage slabs, sidewalks, etc. Let's say 100 yards of concrete for a new house build for a 2,000 sqft house. Current costs would be $21,000 for the concrete plus labor. With the increase it would be $37,800 plus annual inflation costs (3% per year), it would come out to $67,200 for the concrete ($672 per yard) plus labor. Most likely it will be higher, as concrete jumped 40% in just 5 years.

House ownership will be generational (passed down from parents) or only the really wealthy will own houses. The rest of the population will rent and live in densely packed apartment units.

With population growth in the coming decades, a large part of which will lead to housing and other building needs in developing nations, this is more of a challenge than I see indicated in the article. Also some nations are already seeing flooding from taking sand from beaches. We shouldn’t throw in the towel on aggressively replacing concrete as a building material.

Unless I missed it, there was no mention of fly ash as a substitution material in cement. It was all the rage 15-20 years ago but I don't hear it mentioned any more. What happened?

What happened is the decline of coal as a power source. Coal fly ash has been used in concrete for a while, labeled as “supplementary cementious materials.” Conveniently coal was used to fire the kiln that makes Portland cement, if that wasn’t enough coal plants were happy to give it away. Unfortunately, it’s also heavy and shipping it around is not cost effective.

There are still companies out there worlokg its use, but over time it’s not a constant supply chain. Two companies I know of are attempting to make a cement that is based on basaltic minerals, which we already have robust supply chains for, and because it is calcium silicate not calcium oxide making the lime doesn’t release CO2. One company that was on FHB, Brimstone, uses a high temp process to make Portland cement and they passed the certifications. Another, Sublime, uses an electrolyzer and a pH gradient (don’t ask me man, I’m an IT tech not a chemist!) and achieved a performance based cert for hydraulic cement.

iainb,

Interesting!

A former colleague of mine used to run the ash program for a utility with about 8,000 MW of fossil fuel generating capacity. We sent what we could to a Lafarge plant and used to tout how the the fly ash made the concrete stronger. I think it slowed the curing process which increased the strength, but I don't remember. It was 30 years ago. Today there are zero MW of coal generation.

There was also a gypsum plant for scrubber by product to make wallboard. That's also gone now.

They’d pull gypsum out of the scrubber? Didn’t know that. Interesting stuff.

RMI has shared a link to a Technology Review article about Boston based Sublime Systems and their path to a near zero carbon concrete. https://info.rmi.org/e/310101/imate-change-carbon-footprint-/3s3lmjn/1570332808/h/n7G-lhD2Ub3zpo3eMHrR906RH1s4PBD6Zl0JiD-sb2I

The pilot plant produces a minuscule 100 tons/year and uses aggregate instead of limestone as a source for lime. That aggregate is cracked at room temperature using an electrolyzers instead baking limestone at 1600ºC. Using aggregate at low temperature as the source for lime can eliminate about 60% of the CO2 emissions from the start. If the electrolyzer is powered with renewable energy them much of the remaining 40% of CO2 emissions are avoided. A great podcast with the CEO of Sublime Systems with Canary Media's Shayle Kann https://www.canarymedia.com/podcasts/catalyst-with-shayle-kann/fixing-cements-carbon-problem I learned a lot about concrete in the podcast.

David,

Thanks for the links.

Log in or create an account to post a comment.

Sign up Log in