Image Credit: Advanced Energy Economy Institute

More Green Building News

The U.S. government agency responsible for forecasting trends in energy supplies and consumption has “consistently and significantly” underestimated the growth of renewable energy and developed a track record of providing flawed reports to policymakers and planners, a report from the Advanced Energy Economy Institute says.

The AEEI, a nonprofit that promotes alternatives to fossil fuels, released a report this week skewering the U.S. Energy Information Administration for its history of faulty energy predictions.

“Official U.S. government energy forecasts are widely used by policymakers and other stakeholders for analyzing energy supply and demand for long-term planning and policy development purposes,” the report says. “But the [renewable energy] projections bear little resemblance to market realities.”

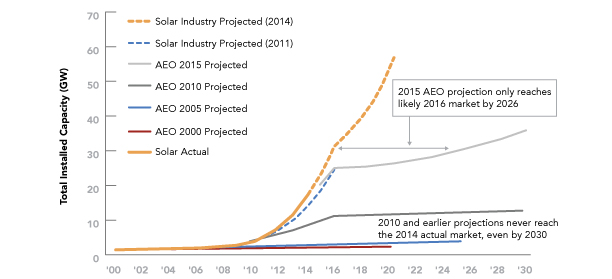

For example, the EIA predicted that installed solar capacity would double between 2014 and 2026 while a market analysis that takes actual projects in the pipeline into account shows that capacity will actually double by next year, 10 years before the EIA said it would, the report says.

“Similarly, U.S. wind installations have averaged about 6.5 GW [gigawatts] per year from 2007 to 2014,” the report adds, “but the 2015 AEO [Annual Energy Outlook] projects a total of 6.5 GW of new wind capacity will be added between 2017 and 2030, less than one-tenth the average rate in recent years.”

The Institute argues that the inaccurate forecasts have raised questions of whether renewable energy and increased energy efficiency can provide “substantial emission reductions at reasonable cost” under the U.S. Environmental Protection Agency’s Clean Power Plan when in fact they could.

Underestimating renewables isn’t new

The pattern goes back at least to 2010, the Institute says, when the AEO projected that the solar market would grow from about 2.5 GW to about 13 GW in 2030. The solar market actually hit the 13 GW mark in 2014, just four years later.

Ditto for wind. The AEO said in 2010 that the wind market would grow from about 40 GW to 69 GW by 2030. In reality, with between 8 and 10 GW of new wind capacity coming online in 2015, total capacity will reach about 75 GW by the end of this year, a decade and a half before the government thought it would.

“As these examples show, AEO forecasts are consistently off by a wide margin, always underestimating — and never overestimating — future deployment of renewables. Such persistent inaccuracy is indicative of a more fundamental problem in understanding the dynamics of growth for these technologies, as well as constraints on how the EIA is required to conduct its modeling.”

The report notes that comparing actual market conditions to predictions for energy efficiency is harder because forecasters must measure something that’s missing — the energy that would have been used were the efficiency measures not introduced.

But the EIA has been off here, too.

“The trend in overall electric demand growth has been consistently downward in recent years, in parallel with the rise in EE [energy efficiency] spending, which more than tripled from 2005 to 2013,” the report says.

Retail sales of electricity have been flat to slightly declining since 2010 even as the economy gained strength. The EIA, however, is predicting future demand growing at a little less than 1% all the way through 2040, “apparently discounting the potential, or likelihood, that EE improvement — through investment and innovation — would continue to reduce demand growth in the coming years.”

Although the EIA would have it otherwise, the report notes that the levelized cost of wind and solar energy declined 58% and 78% respectively between 2009 and 2014 so that renewables are “increasingly competitive with other power sources.” Utility purchases of renewable energy, once based on the requirements of renewable portfolio standards adopted by state governments, are now based on economics alone.

Why are the forecasts so wrong?

Writing at Politico, Michael Grunwald posits that the consistently inaccurate reports are caused in part by “technical constraints” in how EIA makes its calculations. The agency assumes that legislative influences on renewable policies won’t change, when in fact they do.

“But part of the problem is also that the EIA is a prisoner of its own models, which are in turn prisoners of the past,” Grunwald writes. “Wind power was much more expensive than fossil energy in 2009, so the EIA expected it to continue growing slowly. Instead, costs dropped sharply and installations tripled.

“Solar power was cost-prohibitive and virtually nonexistent in America at the time, so the EIA had no reason to expect installations to increase much,” he continues. “Instead, they’ve increased more than 20-fold in just six years, as prices have plunged more than 80 percent.”

In a tweet, he explained it this way: “We’ve had five straight weekdays so according to EIA projections tomorrow will be a weekday too.”

The problem is not just a failure to predict the growth of renewable energy, he adds, but that projections are used to set national policy.

“Unfortunately, the Environmental Protection Agency leaned heavily on those scenarios when devising its Clean Power Plan, which helps explain why the plan’s targets for coal retirements and renewable deployment are so unambitious,” he says.

Weekly Newsletter

Get building science and energy efficiency advice, plus special offers, in your inbox.

{kind=link}

{kind=link}

6 Comments

Great update

Thanks.

Even the EIA estimate of existing PV undershoots by a third!

Since EIA only counts utility scale PV, more than just missing the growth trends, EIA is missing the huge chunk of PV on the ratepayer's side of the meter:

http://www.greentechmedia.com/articles/read/us-solar-electricity-production-50-higher-than-previously-thought

The EIA accounting methods are pretty useless until/unless it starts looking at smaller scale and widely distributed assets, since that's really a major part of the grid future.

The IEA isn't any better (and is in some ways worse.)

Better sources of information

I am glad to see these dinosaurs have been exposed. Many of us saw it years ago. So who should we read for a reality check on the future? Green Peace and the Rocky Mountain Institute have the best track records on renewables predictions. They have been accused of being "dreamers", but in fact even they have not been optimistic enough to keep up with the tsunami of progress in clean energy and efficiency. Just yesterday I read an article on Greentechmedia that Austin Energy had received bids on PV energy for less than 4 cents kwh!! And the expectation is to hit 2 cents kwh by 2018. That is for utility scale solar with the ITC. However even without the ITC they will hit 3.8cents kwh by 2020. And wind? ditto.

Midwestern & Texas wind is still cheaper than 3.8cent PV...

... but PV will become cheaper than wind before 2030, probably before 2025. The fact that PV is more scalable, availalbe, and site-able, it's bound to become the primary new-generation going online within the next decade, despite the relentless learning curve that's happening with wind as well.

Taken to the extremes in super-rich resource areas, wind may be cheap enough to pay for big transmission lines. This completely out-of-scale project has been in the works for getting onto a decade (more power output than a big hydro project), but it remains to be seen whether it (and the transmission line to get it to the richer market) can happen before more locally sited PV & storage eats it's lunch:

http://www.psmag.com/nature-and-technology/how-a-conservative-billionaire-is-moving-heaven-and-earth-to-become-the-biggest-alternative-energy-giant-in-the-country

The fact that both new wind & new PV have already become the cheapest lifecycle cost power in many/most areas means that the lid is about to blow off the can. The exponent in the exponential growth rate of the past decade or two is about become larger.

Forecasting the future is

Forecasting the future is incredibly difficult, but in this case there is also a bias against it by most US government officials and agencies have to tread carefully to avoid being a target of the reality deniers who hold more power and influence then the rational smart people.

All that said forecasting the future is simply fraught with inaccuracy.

It's not nearly as accurate as forecasting the past...

... is it! :-)

The long term learning curves based on production volumes are pretty reliable economic models for a wide variety of manufactured goods. There are no technical or resource reasons why either wind or solar would stall at this point.

Predicting future prices of limited resource COMMODITIES such as oil or natural gas is very difficult, since there are many more moving parts, such as depletion rates, rates of demand rise relative to how fast production rates can rise, changes in the cost of extraction as the resource becomes tighter, vs. techonlogy breakthroughs that lower extraction costs, etc.

By comparison modeling the installed cost of manufactured goods based on production volumes are VERY predictable, but a technology breakthrough on PV efficiency could put a step-function into the short-term cost curve.

With manufacturing learning curves it's production volume, not calendar time that makes the difference. As the price drops below competing technologies/product the production volume ramps accelerate until the market is saturated and it's a mature technology, with flat rather than increasing annual production volumes. We're still at the thin edge of the wedge on the rising tsunami of PV production, and nowhere near the stable year-on-year production volume shelf of a mature product in a saturated market. But now that PV is already cheaper than $10 oil in Saudi Arabia (and winning those contracts), and cheaper than fossil coal in Texas (and winning THOSE contracts), the acceleration is primed to head into turbo-charged mode.

Log in or create an account to post a comment.

Sign up Log in