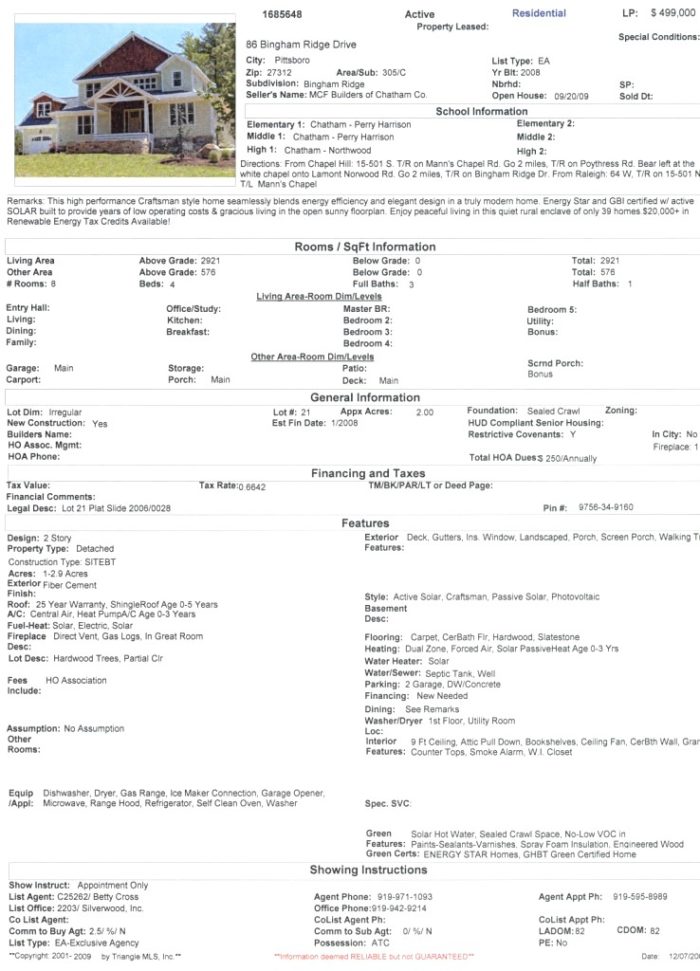

Image Credit: Marsha Burger, EcoBroker

Image Credit: Marsha Burger, EcoBroker Here is the data entry page from our local green MLS. It comes with an index that gives definitions for all the words and concepts referred to here. Contact Green Home Builders of the Triangle, Durham, N.C., to learn more about the process it took to get here. Come to the National Green Building Conference here in Raleigh, N.C., May 16-18, 2010.

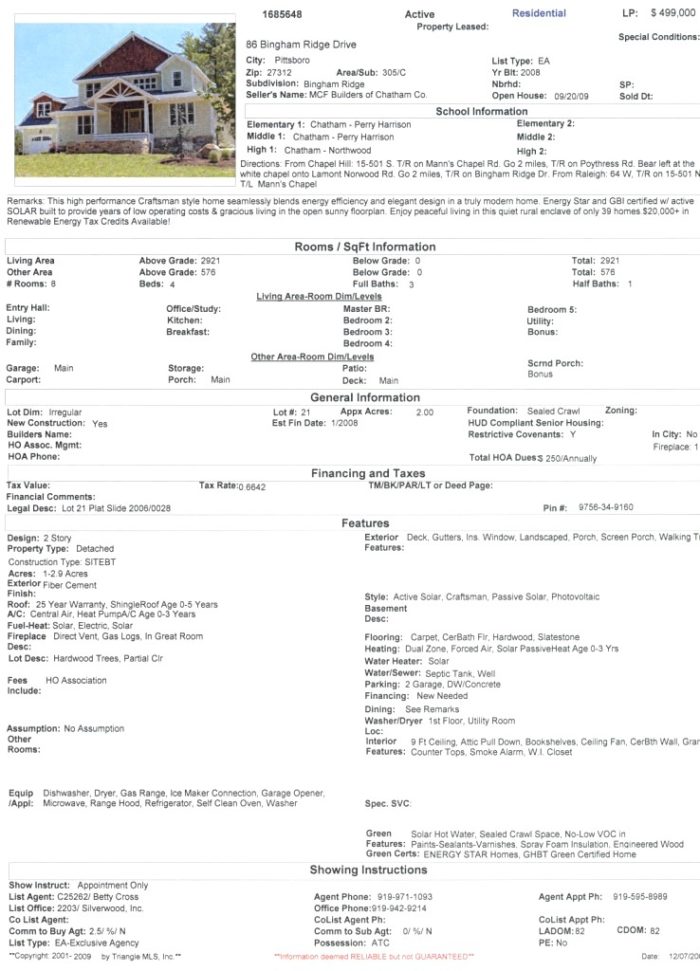

Image Credit: Marsha Burger, Michele Myers, and the GHBT MLS team

More Green Building Blog

I have a customer who is pre-approved for a $400,000 new home. We have the land and a design that fits my customer’s budget. But the bank’s appraiser says that if we build it as designed (passive solar with solar hot water, radiant floor, spray foam in the roof, high-performance windows and insulation), they won’t appraise it for the cost of construction, and the owners will need to come up with a bigger down payment. They don’t have the cash, so we’ll have to eliminate the solar and spray foam so that they can get the loan.

What’s going on here?

Appraising is an actuarial science and a lousy business. For a $300 to $400 fee, an appraiser chosen at random from an appraisal referral service must find other recent resales in a similar location with similar size and features, called “comps,” and draw a defensible conclusion as to the value of the subject property. If the bank’s underwriter in another state finds any inconsistency in the report, they will “kick it back” and make the appraiser correct it at no charge. Only resales can be used as comps; all custom homes are excluded from the MLS database because they “don’t reflect true arm’s length valuation,” in that we rascally green builders can con our poor customers into investing in unproven technologies like solar that might not hold value in the resale market.

So, solar is valued at 50 cents on the dollar, as is spray foam. And if my $400,000 price includes $8,000 for solar and $4,000 for spray foam, the house will appraise for $394,000 and the buyers will need to add $6,000 to their down payment. They’re still pre-qualified for $400,000, so they can add in a Jacuzzi or a home theater if they want, but they can’t have the solar or spray foam unless they can come up with more cash.

Part of the problem is that the appraisers get their data from an MLS that doesn’t necessarily show them what green features are included in the homes that have been sold. Another part of the problem is that most of the homes that have high-performance green features are built as customs on the owner’s land, and these sales are excluded from the MLS. We need a green-enabled MLS and we need a way to get custom home sales included in the appraisal database.

The Green Building Council of our local HBA has been sending speakers to educate Realtors, appraisers, and bankers about green building for quite a while now. It’s a tough crowd, too. But we’ve managed to get a group of the most receptive of them together, and we’ve created a “Green MLS” and implemented it. (Marsha Burger and Michele Myers deserve medals for this.) So now, when homes with green features and certifications are listed in the MLS, those features can be promoted, their effect on the resale price can be noted, and value trends may support lending for green building. The bigger problem of systematically gathering custom home cost data and incorporating it into the MLS for valuation purposes seems much farther away.

NPR recently reported on similar green MLS work being done in Portland, Seattle, California, and New Mexico. We need to take this national. The work of our group is attached to this post; steal it, repeat it, make it better, find a way to get custom homes included. Or we can just keep building and remodeling green for the folks who can afford the big down payments.

Weekly Newsletter

Get building science and energy efficiency advice, plus special offers, in your inbox.

{kind=link}

{kind=link}

35 Comments

Spray foam penalty?

Michael,

Is spray foam the only insulation with an apraisal "penalty"

Or is it any insulation expense beyond code minimum?

Was the foam price for the roof only ?

What is the wall insulation?

I assume you are talking solar hot water

Why should the bank finace solar with a 58 year payback? ;-)

Owner's Equity

Perhaps the apraisal system is not fair.

I say the greenie homeowners should step up to the plate and invest their pocket dollars.

If they believe their operating expense will truly be lower.

Why should the bank take the risk

If they do not have down payment money for a $400,000 house...build smaller.

Extra Square Feet advantage?

Michael,

Does the extra sqaure feet of your extra thick walls give you an apraisal advantage when comparing to comp homes with standard thickness walls?

In north Texas we generally count square footage to the face of the foundation.

In other words .. you say the thick walls only cost you $4,000 extra for one project...

and I would guess that adding 150 square feet should bump your appraisal by more than $15,000

that's an $11,000 impoved apraisal!

Greenie Homeowner comment

I think this is a chicken and egg thing...

People will have to be willing pay more for for better more efficient homes...

And it may have to be as part of the down payment...or more money down.

So the apraisers can justify their numbers.

We need to educate buyers and apraisers.

I don't think people should be so far leveraged into their homes that the down payment will not cover some the good stuff.

I'm assuming a HERS Rating

I'm assuming a HERS Rating was conducted on the house. Could that be presented to the lender? Perhaps you showed them the HERS Rating... If so, what was the bank's response?

Lotta questions here, thanks

The appraisal “penalty” is that there is no increase in valuation for any R-value beyond code minimum, R-15 or R 46? same value. They do recognize Energy Star but don’t differentiate HERS 84 from Hers 46, same value. The bank appraiser will value a home theater, swimming pool, cherry cabinets, and a granite counter top at sale price but green and solar at 50%.

If my buyers choose to build a $360,000 home with $20,000 of green features the bank will value it at $350,000. It’s an option, but they qualify for a $400,000 house and the design we have worked up to meet their needs has already been compromised a lot to fit within that budget.

My goal is for bank appraisers to have a multiple listing service that can quantify sale prices for green building elements in spec as well as custom homes. If they can build a database of what spec and custom buyers who can afford larger down payments are willing to pay to get the green features they want then we could sell this type of product to people who don’t have large down payments. They know how much buyers will pay for a swimming pool or a three car garage, they just don’t have the data to support what people will pay for FSC certified cabinetry and floors, HERS 56 envelope, radiant floor and solar hot water so they are reluctant to lend money to support a premium price for these products.

Many of these things have value to home buyers that exceeds their “rational value” in the same way that luxury tubs and fireplaces do. If our buyers value green building and are willing to pay much larger down payments to get a green built home wouldn’t it be better if the appraisers had a mechanism to recognize that so more people could afford to buy better built, more energy efficient homes that would use less fossil fuels and contribute less to global warming?

I’m not talking about what is “fair” (yuck!), I’m talking about what actions our industry needs to take to create the change that will allow us to build more energy and resource efficient homes for people who very much want to buy them. We need a Green MLS and a way to add custom home sales to a Green MLS database.

2 cents

maybe more than 2 cents. The is a national group to help MLS organizations go green. In Q1 there will be a toolkit and this will help track the green and EE homes, that will help appraisers. Marshall & Swift has a new green cost guide and there is standards that appraisers should follow. my company has developed a course for appraisers and lenders. http://www.greenlendingspecialist.com and http://www.greenvaluationspecialist.com

Good to hear from you Dave

I'll make a point to look you up during the IBS in Las Vegas. I appreciate the work you are doing with the lending and appraisal focus in the NAHB designations. Taking it to the street is what it's all about and you are certainly getting that done. I salute you.

Agents and appraisers

Michael, I know a Real Estate agent who probably has nore than a few words to say on this subject.

I will try to nudge her into commenting here.

Beth Johnson has been a force in turning things around at the MLS in North Texas.

Greening of MLS will happen when...

Don't worry friends, greening of MLS is on the horizon but it’s going to take a while till the entire country does it. I am Realtor in Silicon Valley and have been talking to our local MLS but they say they are waiting for instructions from Cal. Assoc. of Realtors. (San Francisco has done it already as they are pretty progressive there on everything green).

National and Local Association of Realtors are getting very active in this issue and I believe you'll see the change in 2010. Hang in there, it'll happen :-)

Thanks for this article by the way, very good information!

Greening the MLS

Greening MLS systems is indeed a key step to addressing these appraisal challenges. As Dave mentioned and others have mentioned, there is aggressive effort underway to encourage the many disparate MLS services in the country to include green data within listings.

NAR, NeighborWorks, NAHB, USGBC and several other green programs are working together to create a toolkit based largely on the successful greening of certain MLS systems around the country with a goal of providing realtors, builders and other stakeholders with resources to help them approach their local MLS providers about this important issue.

There is a website that already has a lot of good info and more will be added as the tool kit takes shape:

http://www.greenresourcecouncil.org/greening_the_mls.cfm

An Appraisers Perspective

What astounds me is the lack of understanding of appraising real property and the principles of evaluation that need to be adhered to in order to substantiate the value of any characteristic or component of real estate.

What determined the value of a 2 car garage? The market or (typically motivated sellers and buyers in a given market area) by the actions of the market, what the two parties determined by their willingness to pay and sell a property for and what the contributory sales prices reflects the 2 car garage that is a part of the real estate.

This market varies and the demand of buyers varies constantly. It’s not a constant value contribution in every area, in every price range and at any given time.

Principles of contribution, conformity, balance and substitution are some of the principles that appraisers learn and sometimes adhere to in determining value.

For example that garage my cost 18,000 in a region, and in some markets the value contribution might equal 18,000 or what appraisers might say is a cost efficient improvement. Of course the value of the garage might be different for a 800 sq.ft. home than a 3,000 sq.ft. home.

To determine the value contribution the item has to be identified by the appraiser. One column of competing properties has to have homes without garages and one column has to have homes with garages lets say and then some where in the range of the difference in selling prices is the value contribution of the garage.

When there is not enough data or no data at all, then the appraiser has to make a judgment call, or what is referred to as a qualitative adjustment. An adjustment not based on mathematical or statistical analysis but based on surveys done with real estate agents or active participants in the market, or based on their experience if they have any experience or if any of their colleges have experience.

Yet even if you recognize some of the process that is suppose to be completed by the appraiser. There are some basic problems regarding the lack of data or information that is available to the appraiser.

First off every MLS service that I spoke to says that local MLS services choose the characteristics they want to make available to buyers and sellers. That is to say the local realtors don’t feel that the information is applicable for the market, or that they don’t want to fill it out or they simply don’t want buyers to be aware of the differences between homes to make them more energy efficient. So the MLS is not the problem, it is the implementation of the MLS service that is the problem. One MLS service I belong to has a place for energy efficient rating and the other has the potential to disclose it but choose not to.

But are realtors to blame? No in most cases they represent the seller and most of the time realtors don’t want the buyer educated in respect to the cost of maintaining a property because it may negatively impact the marketability of a home or etc.

Real Estate Agents need a budge. For example until the government stepped in or agents started to be sued over lack of disclosure “lead paint disclosures” were not given out. It is part of the system we live in, that we need to get to the point in which energy ratings are at least available to be disclosed, than sellers that want to disclose this aspect of their property can do so and market a possible consideration or asset of their property to the potential buyers in the market.

Then appraisers can have access to this information and consider the value contribution of an energy efficient home or an energy savings component in the valuation process.

But that is not the only concern. Cost systems such as Marshall and Swift do not have a cost option to include in their estimating the cost of a residential property. I don’t agree with David Potter’s assessment of Marshall & Swifts intent. See Below:

Jeff,

Here's a response to your email by the editor of M&S cost manuals.

Right now, the Green section in the Marshall Valuation Service manual is our only source of Green costs available in a unit-in-place cost form. The costs provided are both commercial and residential. The cost themselves do not reflect any particular rating system. They are just components that meet Green standards. We are planning on adding more components to the section for the March update.

We are currently reviewing the best method of adding Green to our software. Since there is no standard formula to become Green, and there are different levels of Green, it is hard to just have a button that will convert the buildings to Green. We do state in our cost manuals that to build Green is about 0% to 7% for commercial and 3% to 20% for residential construction, so manual adjustments can be made.

Let me know if you have any additional questions or comments

Patrick Adkins

Marshall&Swift/Boeckh

Key-Account Sales

Lastly is the inconsistency in understanding energy efficiency and the confusion out there between energy auditor and energy auditor, organization and organization and seller and buyer. If the industry can not collectively determine or agree on certain aspects energy efficient aspects of a property, how are appraisers going to determine a value contribution?

Yesterday I inspected an older home, owned by a commercial energy auditor that has a solar water heater on the roof. The auditor has a damp basement built of granite and rock; there was no insulation on the floor joist or along the sides of the basement. The windows had condensation on them, although it was a problem with the storm windows.

I asked him why he did not address the basement prior to installing a solar hot water heater. He indicated that that addressing the basement like most residential auditor tell you are not very cost effective and those auditors in many cases or emphasis the importance of this characteristic.

He further explained that the SIR or Savings to Investment ration for the solar hot water heater was in excess of 20 years.

So how do I address the solar water heater? Well I can consider it in the overall quality of construction or I can lump it in with other amenities or characteristics of the property. I don’t feel I can note it as an energy efficiency characteristic, because then I would have to bracket it with another property and the MLS does not allow me to search for such characteristic. I can not get it from Marshall and Swift to add to the replacement cost of the structure so I would have to try to find couple of another manufacture or retailers to give me a quote. Which takes up more time than I want to spend or what I get paid for, and the fact is I would get such a large range that it would not be usable.

So as an appraiser, I will acknowledge, consider it somewhere in the report, but the fact is it will not be given the same contributory value as the cost. But by the way neither will the large gazebo on the property. The owner would bet a much better return on his investment if he had built a 2 car garage.

Just something to think about, when discussing appraisals, and the appraisers trying to determine the contributory value of energy efficient characteristics.

LEED Development - Builder FInance Challenge

We are currently in the process of building a 110 home LEED Platinum certified development outside Denver, CO. We have been trying in earnest to secure construction financing over this past year for an initial 5 "Parade Homes" to showcase our "net zero" technologies this August 2010. While we have received kudos from lenders, community leaders and would be buyers on our project, construction lenders remain very cautious to commit. Our development group is subordinating 80% land value, and we have an outside investor group willing to underwrite and subordinate our HVAC systems - which include integrated geothermal, solar, PV and wind. We end up with roughly a 60% loan to value ratio for a construction loan proposition. We are finding that this is the LTV ratio that is breaking the ice with the lenders. Our price ranges are within the $600K - $750K range for these homes. However, even with our large equity portion and reasonable price ranges, the construction lenders coming to the table for this project are requiring a pre-determined "exit" strategy within 24 months to complete the deal. Since these homes are not yet pre-sold, we are trying to determine what are finished product valuations will be at the end and what the permanent lending rules will be in the next 12 - 18 months ----- a VERY DIFFICULT AND FRUSTRATING TASK!

The current market conditions complcate this because foreclosure / short sales on regular buildings are further pushing market values down -- in some instances to below construction cost of typical construction.

Our net zero construction adds roughly $130K - $145K to each home - above and beyond a typical comparable home in the area. The appraisers are not willing to add a dime in valuation. Our realtors, and potential buyers indicate that a 25% price premium would be reasonable and justified for these homes. That price premium puts us in align to cover our extra LEED building costs and eek out a very small (less than 4%) profit.

Although this is not an attractive rate of return, we are in this for the long run -- and hopefully we can demonstrate value.

My questions --- Given the 30% tax credits available on qualified systems, and integrated building materials, Must not the appraiser need to factor that in on final evaluation --- since these are hard quantifiable dollar amounts that are realized to the buyer? Also, if we can provide a verifiable database of energy savings to comparable homes in the area, why can't that be used to build a net present value number to be added on to valuation?

If the home owner is not spending $ in utilities per month, they have additional $/month to go toward nome mortage financing. It appears that the commercial real estate sector is beginning to incorporate this into leasing and sales rates/ values ----- why can't this be taken similarly to the residential market? Even though adequate comps are not readily available in any given market for green/LEED buildings yet; alternative & proven financial valuation models are readily available that can be incorporated and solidily justify valuations for appraisers and lenders.

As the market is beginning to require and adjust to energy savings buildings, the appraisal community and lenders will be forced to adjust to new valuation methods -- other than comparables. Utilyzing comparables valuation is now becomming a flawed method and will soon render appraisers and lenders relying on such valuations as irrelevant.

Are you aware of any MLS database in the country incorporating any information on $ savings for the buyer / realtor to do comparative analysis?

LEED development

Mark

I feel and share your pain. There is a proven market for LEED, net-zero and passive-house but actually getting these projects financed is subject to the availability of people willing to put more than 25% down to compensate for appraisals that don't come up to market value due to lack of differentiation in the appraisal and MLS system for high performance options.

I spoke with Sam Rashkin from Energy Star about it this fall and he suggested that, since the HERS report can include an energy savings calculation, those projected savings could be back-calculated to compare to a similar principle increase in the mortgage and equate to an increase in the valuation, this approach is similar to the current energy efficient mortgage programs. The calculation would have to be laid out in the plans and specs for the appraiser, as would any prospective tax credit. When you ask about who is doing this I think a good place to start would be Bob Hartford and Betty Cross at http://www.silverwood-inc.com/Bingham_Ridge_Home_Page.html who have a pretty good track record on this sort of development through our local Branch Bank and Trust. I also note that Wells Fargo is pursuing the green home market fairly aggressively.

Jeff Patterson makes a good point about the relative value of the same investment in an gazebo as compared to a two car garage. We all need to understand and accept that market value and cost of construction are very different things and that we cannot expect that appraisals will reflect cost of construction instead of market value. But if we have buyers who are willing to pay a premium for high performance building systems we need to modify the MLS to capture that market value and allow banks to loan money to support better than code construction rather than just go along with a system that limits innovative homes to people with very large down payments. At present these buyers can't find the product they seek in the speculative housing market because the banks can't loan to spec builders for high performance homes due to the low appraisals so those buyers are building custom homes through lucky guys like me but those sales don't get added to the MLS and so the appraisal problem continues and mainstream spec-builders and buyers are forced to settle for near code-minimum construction.

Fixing the MLS is just one of the first steps.

Houston MLS has added green certs & e-efficiency

Interesting article.

It may surprise all to learn that I worked with a task force at the Houston Assoc of Realtors to create and implement a green certifications input, as well as a comprehensive list of energy and green building feature inputs (including almost all types of insulation used), all which are now in MLS and being used. As a matter of fact, we are starting to see many new construction homes take advantage of thse features, and all my new construction listings in the Heights are listed with spray foam inputs, Energy Star inputs, etc. MLS reports adoption is slow but steady. This has been up and running now for about months.

I also give regular talks to brokers in Houston about green and energy efficient issues. The National Association of Realtors developed a fairly comprehensive two-day curriculum (NAR GREEN) to certify brokers as knowledgeable of sustainable building practices, and I taught the first of these courses at HAR last year. Hopefully, we will see more of these classes this year.

Erik Fowler

(713) 398-7948

http://www.efowler.com

-Residential Real Estate Brokerage & Consulting / Realtor®

-LEED Green Associate, Eco-Broker®

-Greenwood King Properties

-Top Houston Realtor - HTexas Magazine 2005, 2009

-Board Member, Greater Houston Chapter of US Green Building Council

Houston MLS codes green last year - article

http://houstonrealtor.har.com/DispArticle.cfm?ARTICLE_ID=26342&ISSUE_ID=2007&KEYWORD=green

HHI should be added to home listings

Real estate folks, including MLS, should consider following the newly adopted provision in the 2006 edition of the International Residential Code (IRC) which requires that a permanent certificate stating the home’s energy efficiency information (R-values, U-values, solar heat gain coefficients, etc.) be posted on the electrical distribution panel. This same information, along with HHI-SHELL and HHI-MECH, should be entered into a data field in the listing. In fact, for simplicity, maybe just the two HHIs (Home Heating Indices) should be included.

HHI-SHELL is the number of BTUs per square foot per heating degree day (BTU/sf/HDD) the structure’s shell requires to maintain comfortable temperatures in winter in the local climate.

HHI-MECH is the BTU/sf/HDD of imported energy that the mechanical system must have dumped into it to provide the shell with what it needs. HHI-MECH is higher than HHI-SHELL because some heat goes up the chimney. So, HHI-MECH is almost a direct measure of heating costs for the house.

When shopping for a house, the house with the lower HHI-MECH IS the more energy efficient house. HHI-MECH is equivalent to the EPA MPG for vehicles, and is an excellent basis for decisions related to future energy costs for heating the house.

Of course, how the occupants “drive” the house and how much energy THEY use can make an enormous difference, but the underlying energy efficiency of the house is unaffected by long showers, big screen TVs or thermostats set to 75 degrees in winter.

You would think that a Home Cooling Index (HCI) for the summer cooling season would be required also, but it is not. The HHI and the HCI correlate so well in most areas, that only the HHI is required to compare the energy efficiencies of houses.

The HERS index is NOT a good measure of energy efficiency. It mixes home energy efficiency with occupant choices/behavior and with energy generation. Under HERS a house with very poor energy efficiency (e.g., major heat losses through the shell) can have a HERS of zero (0) with the additions of enough solar photovoltaic panels. So, HERS can’t be used as a true energy efficiency measure.

For more information on HHI see

http://www.homeenergy.org/article_full.php?id=612&article_title=MPG_for_Homes

Appraisals

I agre this effort needs to go national. My partner and I are struggling with the same issues which are squeezing or profit margins on spec homes, all of which are built to the NAHB standard Silver level. In addition I work full time at a bank so I understand this from an additional perspective. We have to realize that the appraisers have a set of guideline they have to follow. On of the best ways to attack this is to get FHA & VA to promote green building in such a way that directs the appraisers to add to the cost of green features to homes that they finance. FNAM & FHLMC would need to be directed to follow suit. If the administration is serious about energy efficiency they need to be a facilitator not an inhibitor.

My Recent Apprisal

I have 4.3KW solar electric system for my energy star house in Maryland.

Which cost me $30K to install solar system. Last week we did appraisal to refinance my mortgage. Appraiser did not add any value for solar system or energy star features.

I am thinking to challenge this appraisal since he did not added any value for solar system, is it worth it?

Here is the HUD document to consider solar systems.

http://www.hud.gov/offices/adm/hudclips/handbooks/hsgh/4150.2/41502appbHSGH.pdf

Your recent appraisal

Raju

this is exactly the issue we are attempting to address here. You can certainly show the energy cost saved annually from the Energy Star report and the energy produced by the solar array and ask to have that value considered in the appraisal. (given the long payback of solar at today's energy prices you will be lucky to get 1/3 value on that method of valuation) But the easier route would be to shop the loan to a bank that has a residential green lending policy such as Branch Bank and Trust or Wells Fargo if either of them are serving your area.

At issue is that the appraisers are at the mercy of the banks underwriters so if they show value for green features that they cannot show comparable re-sales for the under writers can, and will kick the appraisal back on it and make them do it over again. A typical appraisal in our area earns a $350 fee to the appraisal business, so more than one kick kills their profit margin. If the bank has a reputation for having tough underwriters the appraisers just won't show value for anything they can't show a comp on. Until we have a green MLS and a history of green re-sales there is no way to show green comps and accurately evaluate the market value of green features.

The HUD document is useful, maybe your bank will come around but I would bet on shopping the re-fi to a more green friendly bank. Good luck with that, perseverance and equanimity will be required on that one.

No Luck - My recent appraisal

Michael,

No luck with my recent appraisal, Here is the response from them:

We have investigated the issues raised, concerning the solar panels.In our discussion with the appraiser, he indicated that he would have liked to have made an adjustment for the solar panels, but there is absolutely no market evidence to support any adjustments. The appraiser can base adjustments on a calculator for a different market, and per Fannie Mae, if there is no market data to support an adjustment, then no adjustment should be made. Even though we all believe an adjustment may be warranted, an appraiser is bound not to make one, if he cannot support that adjustment with verifiable data. This is appropriate and reasonable appraisal practice.

Sorry to hear the bad news

Raju,

I think that you and Michael Chandler are pointing to a real problem — one that is usually ignored by the green building community.

To be honest and realistic, it's important for green building advocates to admit that green amenities may not be reflected in appraisals. It's also important for us to continue educating the general public, in hopes of raising the value of homes with green amenities. Only when home sales prices reflect these green improvements will the attitudes of appraisers change.

refi appraisal with 6kW Solar PV $0 credit!

I am quite frustrated as I just had my home appraised for a refi. I have installed a 6000 watt PV on-grid Solar Array. The appraisal company refuses to give me any credit for this $36000 investment whatsoever! I have been given the run-around by the appraisal company (metro-west appraisal co llc in scottsdale AZ) and the lender (quicken loans). I have given up on this particular refinance as I need to close by 4/1, but certainly wish I would have anticipated this obtuseness right away so that I could have perhaps pursued a more "green friendly" lender and appraisal company. This is a great resource site, I will not give up this fight!

The big question

The big question through all this discussion is: How much will the consumer pay for Green? Will home buyers in Denver risk an extra $135,000 plus the developer's profit to save energy? Get a buyer and have that buyer discuss their decision process with a competent professionally designated appraiser who understands and has taken the Appraisal Institute's seminars on the subject. Don't hold back any information. Appraiser's generally measure market activity, not cost to build. There are many improvements to a home that immediately lose money , like a swimming pool, or over the top finishes. Consumers will pay more than costs for some items, actual cost for others and less than cost for those items that go over the top. Appraising 101, teaches that cost does not necessarily equal value. So if there is a positive value effect, sit down with a specialist appraiser and talk it over. Everybody is making this hard by choosing idiot appraisers from pool of licensees who received their credentials when licensing took effect. All appraisers are not equal. Choosing an appraiser is the key. But, the good appraisers are not willing to work in the low bid pool of appraisers that the lenders are using now, just the idiots working out of their basements.

Choosing appraisers

Richard The recent banking changes no longer allow bankers or builders to select their appraisers. We are now required to have the appraiser selected by a third party broker from a blind pool and the banker is not allowed to talk with the appraiser. On the job discussed above I did hire a green savvy appraiser (at significantly more than I paid for the real appraisal and brokers fee) to consult on the plans to help us get the value to cost ratio up to where we needed it to be to make the project work with the limited down payment funds available. The appraiser who did the actual appraisal was not from our market and was completely un-familiar with green building and could only use information on cost comparables from the MLS in his computer. This is why an MLS that reports accurately on what buyers are willing to pay for green features is so critical.

Thank you.

We are currently dealing with this on our DER project in Cleveland, OH; I'm hoping that a local push for energy-efficiency will help improve appraisals for others (and hopefully our house in the future).

Green appraisals

Bank loans are almost always resold through FNMA. FNMA rules thus set the standards. Currently the rules, as interpreted by underwriters, require a sale of a similar characteristic in a comparable. If such a sale doesn't exist, a reasonable rationale for a valuation may be advanced.

So a percentage of cost for a DWH that was returned in a sale may be analyzed and shown to be a reasonable expectation for added insulation, as an example. BUT, as mentioned, if appraisers can not determine which sales had green features, they can not advance any argument, even if they want to.

Appraisers do not make the market, they reflect it. Once the buying public demands information on "greenness", then MLS will put the information in the form. If the builder wants to help appraiser reflect the value, keep track of prior sales and present them to the appraiser. Until data can be presented to appraisers and underwriters that there is public willingness to pay, it won't be recognized in appraisals.

If you want the feature, you have to pay for it by accepting the risk yourself.

I was willing to pay for it!

I have read this entire thread, and a constant theme is that buyer's have to be willing to pay for green. Well, I was. I signed a contract to buy probably the greenest house in our county in rural North Carolina for $257,000. I thought it was a very good price for a house that had custom everything, will have next to nothing in utility bills, and should be in great shape 100 years from now. My wife and I have a professional jobs, a 150K+ household income, and 800 credit scores. The appraisal came back at 225,000 and killed the deal. Even if we put in the difference in cash, THE BANK WOULD NOT LOAN US ANY AMOUNT TO BUY THE HOUSE UNLESS THE HOUSE APPRAISED FOR THE CONTRACT PRICE. Sorry about the obnoxious capitals, but reading this thread reminded me of how much this incident pissed me off. We had a time crush as well, so couldn't try to work out another way to finance the house.

And, I was right in the middle of building a couple of green townhouses (just good blown-in insulation, composite decking, 50 year siding, 50 year shingles, mini-split heating/cooling, wired for solar, Healthy Built Home Gold--nothing over the top) and I was lucky enough to draw the same appraiser--I protested, but in vain-- and the final appraisal came in 30,000 under cost to build, and 20,000 under the pre-construction appraisal (different appraiser). And I built them for $135 a square foot. Of course he made no adjustments for energy efficiency or low maintenance costs.

So I strongly affirm all that has been said about getting these green features recorded to provide a database for comparison. But my bigger point is that appraisers, and this appraiser in particular, need to step up and do the right thing. I have seen enough appraisals to know how highly subjective they are, especially in a place with not very many comps. Appraisers don't just reflect the market, they either help create the market or help kill the market. If appraisers want to create some value on an appraisal, they know how to do it. Now I will have to advise everyone I know who is going to build to stay away from green if they are ever going to need an appraisal to close on a loan, refinance, or sell their house--which means about everyone.

Somebody in power needs to fix this problem now--it is crushing any possibility of green construction in our county, and it sounds like this is far too common of a tale.

Willing to pay

This is a pretty rough tale. It's not uncommon for banks to require thirty percent or more cash down for green homes but I've yet to hear of a bank that wouldn't loan 80 percent of the appraised value even if that was far less than the contract price. Times are getting tough and banks just don't seem all that interested in loaning money for any reason.

Our own house was threatened with foreclosure because the bank increased our escrow but didn't notify us so our mortgage auto draft came a little short every month. after three months of being $26.00 short on the auto draft they started calling us at work but wouldn't say who they were trying to call or what it was about, only that some one at this number needed to call Wells Fargo with their loan number in hand to straighten out a problem. We asked around and finally figured out that it had to be us (we were on auto draft so we figured it must be one of our employees) by that time they were threatening us with foreclosure and we were still less than a eighty dollars behind. Then, of course they made it extremely difficult to pay and wouldn't give us a direct phone number so every time we called back we had to wait through interminable voice menus. Here I thought Wells Fargo was one of the better banks.

I feel your pain. The economy stinks and the banks are crushing any chance for recovery.

There are qualified appraisers

Michael, There are qualified appraisers to value these Green Built & High Performance Energy Star Homes. There are a myriad of barriers at this time in the Real Estate Market. The appraisers that are qualified are many times blocked by Lenders who will not allow a new appraiser on to their appraiser rotation. Appraisal Management Companies do not always pick the appropriate qualified appraisers to do these assignments. They are looking for the cheapest appraiser who typically will not do the additional research needed to find appropriate comparables, etc. The Hers raters do not always return email or phone calls to the appraiser to establish the HERS rating of the subject or comparables. There is no one stop shop to find the Green Level Certifications or HERs ratings at this time. The builders don't always advertise or market their Green Built Home or Energy Star High Performance home with appropriate certifications. The Realtor may not market the home correctly on the MLS site. Many Lenders are not even addressing these Energy Efficient Mortgages. Due to low fees offered by the AMC's, you get whatever appraiser is on rotation who just wants to get this appraisal done. The appraisal industry is finally starting to acknowledge Green Built, Leed, and High Performance homes. My company and staff have taken classes thru the Appraisal Institute and are now GreenValuation Speicalists thru Porterworks. Appraising Green Homes.........is considered to be a complex assignment therefore; only a qualified appraiser should be allowed to appraise these Green & High Performance Homes. You may request your Lender find an appraiser that is qualified. Until, Lenders, Realtors, Builders, MLS, Raters, Inspectors and Appraisers are educated and recognize this Energy /Green market it will take time for these changes to be implemented. An appraiser is able to address Quality of construction differences between a Traditional Built Home to a Leed or NAHB Green Built home. It just takes additional time & research. When appraising a High Performance Energy Star Home the appraiser should utilize the HERS rating or Gross Rent Multiplier to make an adjustment under energy efficiency in the appraisal grid. As long as an appraiser does the necessary additional research, brackets a Green Built, Leed or Energy Star home, utilizes research data available on (internet, MLS, public records,Builder information) the appraiser should be able to do a quality appraisal. The HERS rating, Green or Leed Level will eventually need to be permanently affixed to the county public records so the appraiser will have the data needed to value these homes. Many realtors do not adequately market these homes in the MLS site so, the best place for permanent records is the Public County Records. This will be especially true for resales and refinances. The appraisal will know then it is Green Built or Energy Efficient. Karin Argeris

Thanks Karin

I just want to say thanks so much for your indefatigable work on this issue.

I often refer my past clients prepping a house for re-sale to your company because i think it does make a difference when you have a positive appraisal as part of the sales information package even if it's not legally allowable to the bank, it gives whatever appraiser gets assigned by the appraisal management company hired by the bank an easy place to look for the information that shouldn't be so hard to find.

Green Building Appraisal & Financing issues

I'm getting into this discussion very late, but here it goes. I have been involved in a valuation project, along with a fellow appraiser in Nevada City, CA, Debra Little. We have been asked by Build It Green and The Energy Coalition as part of their Home Energy Make Over Contest to develop methodologies to value the premiums from Green Upgrades. I have been working on 3 single-family homes in L.A. County.

I second Jeff Patterson's comments about what residential appraisers are up against in valuing these types of properties. Residential appraisers today are not paid enough, nor are they being given enough time to complete competant appraisals of such a complex property. I don't wish to jump on my soap box about this issue for this post. Please contact me & I'll be happy to discuss what borrowers, buyers & investors are up against in trying to get a reasonable appraisal analysis.

For our currrent project, Debra & I have been working for the last three months on the three properties in our market study. I have developed four mathematical models that I am using to act as a proxy for the actions of buyers and sellers in order to estimate the premium for which properties should sell. I will be happy to share my write-up with anyone when I complete it.

I've interviewed two dozen Agents during my research, and there has been a lengthy discussion on several of the Appraiser Forums to which I belong about this isue. Both appraisers and agents generally lack any knowledge about the valuation of Green properties because it is so new in the So. CA area.

In the MLS Boards, I have searched for general terms like "Green" in order to try to identify. The results that came up included "green" houses and "green" grass, nothing about Green Upgrades. II also searched for "LEED" , "Energy Efficiency" and other terms. Search results included: Energy Efficient hot water heaters & HVAC systems. The point is that until there is a cogent way to identify properites with Green Upgrades AND have Agents add the Performance Reports into their listings, along with the specifications of the Solar Systems, base line energy costs BEFORE installation, and savings AFTER installations, we appraisers will never be able to compare properties or apply the mathematical models I have developed.

Debra & I have had it easy in one respect. We haven't had to worry about some Underwriter, AMC or Lender shooting down our findings just because there aren't any specific sales of Green Upgraded proeprties. If you read HUD's 4150.2 - Appendix B, Special Programs - See Raju's post above, HUD allows a bump of up to 20% above insurable levels for Solar Energy upgrades.

To end this post at this time, all of us working in this arena have to ensure that much more data becomes available before appraisers can apply premiums for energy upgrades.

John C. Carlson

http://www.jccrea.com

John - I agree we need data to make value assessments

We need green elements on the MLS

We need to train agents to check of those elements accurately

then we can start to analyze how the elements impact re-sale

The we can get the data to support increased valuations for Homes with green elements.

It's complex - Thanks for your input.

Help IS on the way for valuation of green buildings

Later this year (2012) the Journal of Sustainable Real Estate will be publishing a groundbreaking paper for North America that will halp appraisers better handle the valuation of green buildings - the paper is entitled "Sustainability and Income-Producing Property Valuation: North American Status and Recommended Procedures."

National changes coming & supplying more data

First, I learned the following from The Appraisal Foundation this summer:

Through a 5-year Memorandum of Understanding with the US Department of Energy, The Appraisal Foundation is very much incorporating the valuation of green buildings in the work of our three independent Boards: the Appraisal Practices Board (APB), Appraisal Standards Board (ASB), and Appraiser Qualifications Board (AQB).

The APB has begun the process of providing guidance on recognized valuation methods and techniques of green buildings with the creation of its first Subject Matter Expert (SME) panel on the topic, Background Competence. The APB intends to create two additional panels: Valuation of Residential Green Buildings, and Valuation of Non-Residential Green Buildings.

The AQB adopted revisions to the Real Property Appraiser Qualification Criteria that will become effective on January 1, 2015, which will require individuals wishing to obtain an appraiser's license or certification to complete qualifying education in the valuation of green buildings, and for those who already possess an appraiser credential, continuing education related to the same topic. A brief summary of the 2015 changes can be found by clicking on the following link to our website:

https://appraisalfoundation.sharefile.com/download.aspx?id=sd2f26fafefe402ab#

Lastly, the ASB will issue guidance related to complying with the Uniform Standards of Professional Appraisal Practice (USPAP) when valuing green buildings.

*****************************************

I found the information above to be very useful in conveying to our state regulators and appraisal association that this is inevitable and the sooner we get the educational support going the better.

Second, we have simplified the greening of ME, NH, and VT's MLS. The features added include a Home Energy Rating Index Score, and 3rd party building certifications (ENERGY STAR, LEED for Homes, National Green Building Standard, etc. - also the LEED and NGBS certification choices show the actual rating achieved such as Platinum, or Emerald). Basically we want to focus on the bottomline as opposed to the component parts. Like many acknowledged, our best homes don't show up in the MLS as they are custom homes and not the "arm's length transaction" the appraisers want. So in VT our ENERGY STAR sponsor, with permission included on our enrollment form, is now providing our region's MLS provider with the physical address, HERS score, building certifications earned, and date built for all projects that participate in our statewide efficiency and/or green building services. The intent with this simple Excel database is to provide appraisers with a larger pool of homes to use as comparables. We hear up here too that our new homes are resold in 7 years on average. Eventually this searchable data may pick up today's homes when they're resold. We are now reaching out to the other NE states to encourage them to use these features.

Log in or create an account to post a comment.

Sign up Log in